Bouvet: Sleeping Compounder

Norwegian consultancy w/ 27% CAGR for a decade, despite being flat for the last 3.

Commentary: Over a long enough time period, a stock-price follow the fundamentals of a company. However, for long stretches, the valuation can move ahead of the fundamentals, and the stock may need a little breather for fundamentals to catch up. In this writeup, I will uncover a Norwegian compounder which has been in this stage for 3 years now. While sentiment among retail investors suggests many have lost faith, today’s risk/reward may be favourably tilted for the long-term investor.

A quick look in the rearview mirror

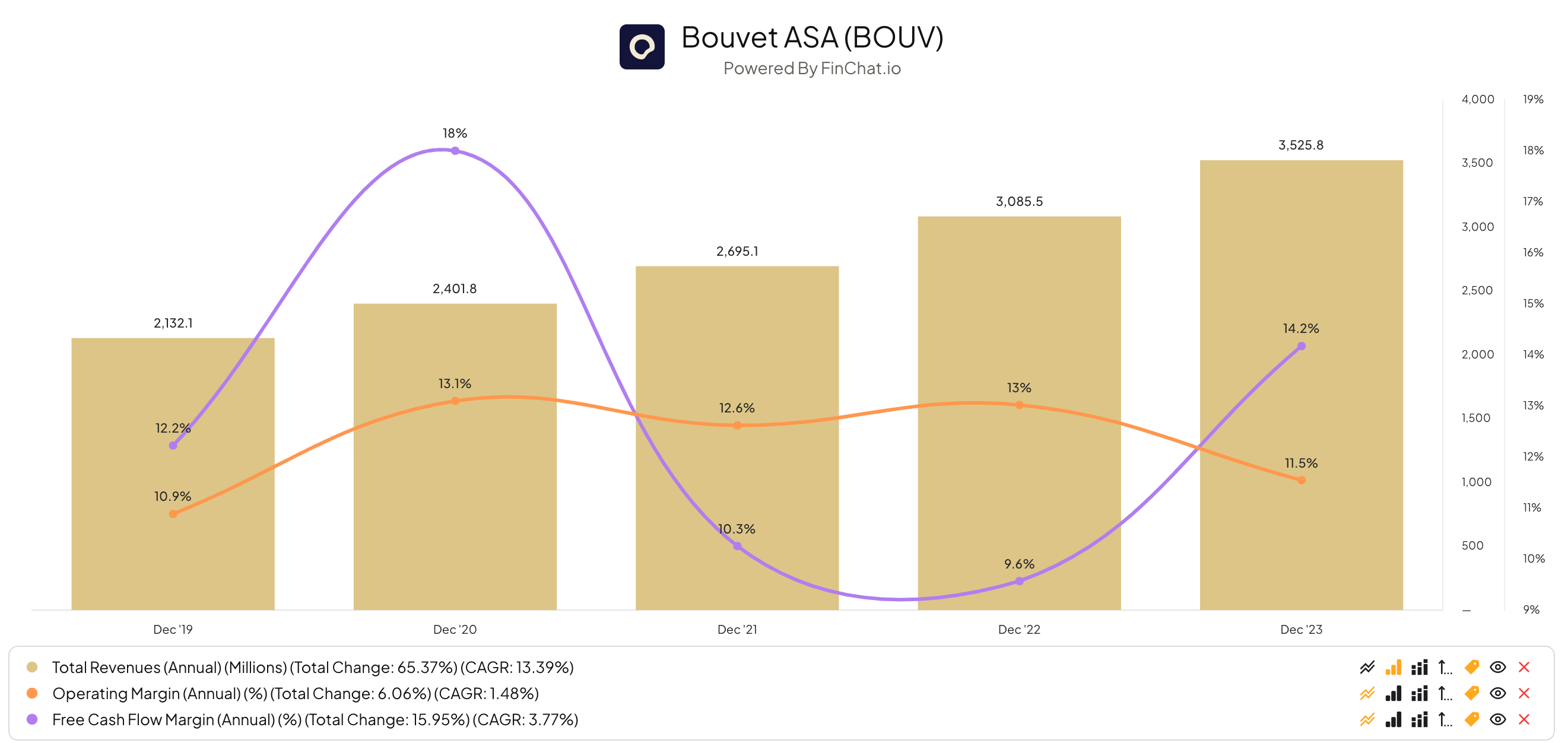

As you can see per the graph below, Bouvet´s fundamentals are ticking upwards, with growing top-line and relatively strong margins. As for many companies, the cashflow moves in cycles and should even out over time.

Despite the fundamentals developing nicely, the stock price have delivered no returns since 2020. Breaking down the 3 components behind shareholder returns, it´s easy to see why:

Earnings per share: +33% (+46% Revenues & Net margins 10% → 9%)

PE Multiple: 29x → 19x

Dividend yield: Average of ~3% (payout ratio ~85%)

When combining these factors, the calculation yields 1.33 * 0.65 + 4 * 1.03, resulting in an approximate return of 0%. The discrepancy between the strong fundamentals and multiple compression may stem from several factors, such as diminished confidence in the consultancy industry, shifts in investor sentiment away from Norway, or just the stock markets voting mechanism taking a breather from Bouvet´s fundamentals.

A competitive industry

The consultancy sector remains competitive and densely populated, a trend likely to persist. Characterised by minimal capital requirements, primarily comprising salaries and office leasing, it operates as a capital-light industry, facilitating ample dividends to shareholders.

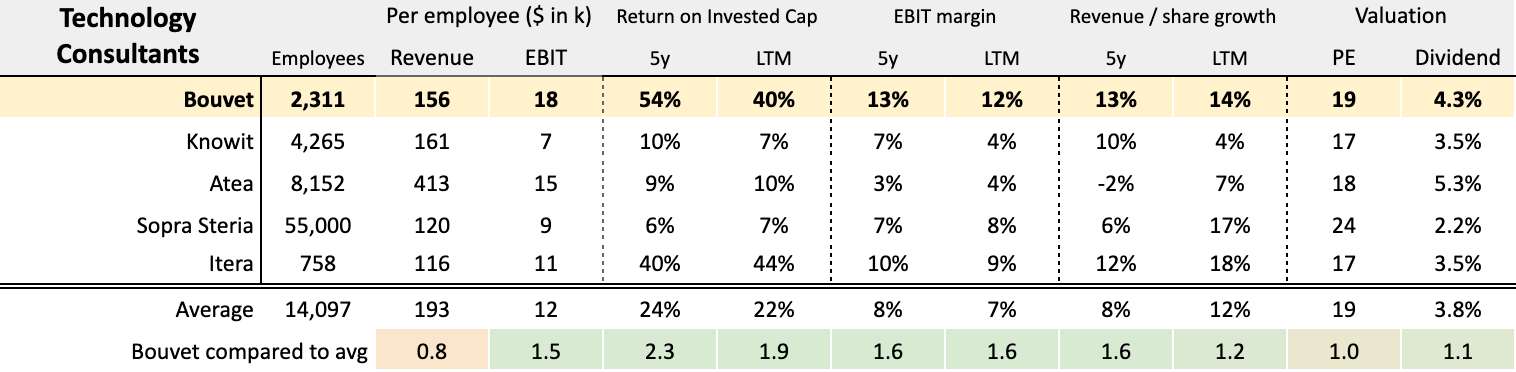

Looking at peers of varied size, as illustrated below, Bouvet stands out as the one of highest quality. Higher margins, improved capital efficiency, steadier growth & higher profit per employee. Surprisingly, at a similar price point.

So, what make Bouvet´s numbers resemble higher quality? CEO, Per-Gunnar Tronsli, called out something interesting during the Q4 call. They see heightened competition for new project bids, leading to lower revenues and margins per new client going forward. However, >97% of Bouvet´s revenue came from old clients this year. This has been a core pillar to Bouvet´s strategy since the beginning - develop deep & growing customer relationships. It makes me think of a quote from mr. Terry Smith: We make most money with old friends.

Digitalisation is a crucial factor in today’s society for the delivery capability and competitiveness of enterprises. Our many years of experience, closeness to clients and broad expertise make us a very attractive digitalisation partner for both private and public players (Q4 23)

The competitive edge

As Bouvet emphasises, digitalisation is about preparing for the future every day. Their potential success relies on several components:

Digitalisation: Represents the opportunity for growth and innovation.

Closeness to Clients: Building deep, lasting relationships with clients serves as a competitive advantage.

Broad Expertise: Bouvet's diverse expertise enables them to address a wide range of client needs effectively.

Competing against Bouvet for a contract means competing against a company with employees who have spent years, potentially a decade, working within organisations like Equinor. This firsthand experience gives Bouvet a competitive advantage, allowing them to compete based on their ability to solve core issues, rather than solely on price. Leveraging these relationship and understanding of their customers problems, Bouvet maintains a distinctive position in the market. Similarly, there would be a concern if Bouvet were to lose some of these longstanding customers. Additionally, expanding beyond these key clients may expose them to a more competitive landscape, characterised by (more) intense pricing pressures prevalent in the industry.

Moreover, Bouvet has recently concluded a smaller acquisition (Headit, 1.5% size of Bouvet). The successful integration of new employees and clients will be crucial, particularly if acquisitions is set to become a primary focus of capital allocation in the future.

Thanks to their loyal (and growing) customers, new Bouvet employees (experiencing 14% growth in 2023) can seamlessly integrate into existing client work-streams. Tronsli commentd on this during the Q4 call, observing that new hires typically transition to invoicing within only days or weeks, a timeline previously spanning closer to months.

Resilient Clients

A quick look at their customer list below, reveal resilient organisations - built to withstand the test of time. These include entities like the police, national defense agencies, airport operators, and energy giants. It's noteworthy that Bouvet's significant reliance (41% of revenues) on clients like Equinor, Aker BP, and Repsol positions Bouvet akin to an oil-service business, supporting a critical pillar within the Norwegian & European energy economy. Interestingly, they assist these business in both their current operations and, for transitioning into renewables.

Type of Projects & Sector Tailwinds

Bouvet's project portfolio encompasses a broad spectrum, ranging from developing robots for airport tarmac inspections, to streamlining court filings administration or crafting algorithms for train energy consumption. Later, we'll explore how emerging technologies like Artificial Intelligence, present opportunities for Bouvet. Leveraging its diverse competencies & experience, Bouvet assists large organisations in solving complex & core issues.

Two sectors currently experiencing significant decade-long transitions are Power Distribution and Oil & Gas, as seen in the accompanying graph to the right. Notably, revenue growth in these sectors has surged, with figures increasing from 109 to 181 million NOK in Power Distribution and from 162 to 394 million NOK in Oil & Gas since 2020. Consequently, one could argue that these sectors have absorbed most of the new hires, seen to the left.

Artificial Intelligence → Risk or opportunity

When we think of AI, a common concern is its potential to replace jobs. While this may hold true in some cases, companies are increasingly turning to Bouvet for AI solutions, highlighted by Tronsli during the Q4 call. Asking ChatGPT about the readiness of a certain airport tarmac, is quite different from asking it to compose a poem. While the airport tarmac is a perfect place to deploy AI technology, with it´s excellence in pattern recognition, it still requires a lot of customisation to work within a field with high stakes at play. “Out of the box” solutions don’t always work in real life. Microsoft, the owner of ChatGPT, grants Bouvet's customers early access to most of Microsoft's cutting-edge technology, by being their preferred technology partner.

Despite being at the early stages of this revolutionary technology, Bouvet already leverage AI for tasks like developing pattern recognition for law enforcement or trading mechanisms for energy consumption. These solutions will likely always necessitate customisation, collaboration, and innovative design to meet the needs of all stakeholders. However, there's the possibility that certain tasks could become highly automated, allowing well-articulated prompts by employees to address challenges or streamline processes, potentially reducing the demand for consultants in certain areas.

Nevertheless, for every problem AI solves without human intervention, there may arise just as many opportunities to deploy AI to augment human capabilities. With Bouvet´s customers coming to them for assistance, they are in pole position to adapt to the evolving landscape.

The compounder waking up

Simplifying valuation for a company like Bouvet seems prudent. The current price to earnings multiple of 19, appear cheap for a business offering >4% dividend yield alongside growth prospects. Further, Bouvet's historical growth have required minimal capital, boasting a robust >40% return on invested capital (ROIC). Assuming a continued annual headcount growth of ~10% per year, and a revenue per employee increase similar to inflation targets (~2%), a top-line growth of approximately 12% could be achievable.

As consultants usually exhibit no operating leverage at scale, I would assume a regression from historic averages in operating margins to ~11%, in line with current conditions. This scenario would imply an annual EPS increase of ~12%, combined with a 4-5% dividend yield. Such a scenario could be appealing to long-term investors, especially as a lower valuation multiple would position $BOUV closer to non-growth companies or those with ROIC much closer to their cost of capital. For now, Bouvet seem to be able to grow within (primarily) existing clients, this may change in the future.

Alternatively, if one believes Bouvet merits a higher multiple, say closer to a 25 PE ratio, there's even potential for a 20%+ compound annual growth rate (CAGR) over the next 5 years. This projection factors in 12% EPS growth, a 5% dividend yield, and an additional 25% total return from multiple expansion. Time will tell how growth and multiples will look like, although, today´s price of 19 does not seem to price in anything close to this growth.

For investors outside Norway, the depreciation of our currency may be an unattractive prospect, and a potential reason for Bouvet´s multiple. I will not spend time predicting future currency movements, as this is well beyond my knowledge. Although, I would not be surprised if our politicians could increase corporate tax-rates further & potentially, scaring outside investors further away.

Wrapping things up, it's essential to acknowledge that both fundamental factors and stock prices can go way higher or lower from today´s levels. As always, none of this constitutes financial advice.

Disclosure: I do own shares of Bouvet. Sources used in this writeup, is mostly Bouvet Investor Relations documents & earnings calls. If you are interested in Bouvet, I would recommend starting there & also take a look at their annual report for employees. Gives good insights to the type of projects they work on, and their corporate culture.