Shift4: All Pieces in Place

What may seem like a conventional payments terminal operator on the surface, mask a deeper reality - The unlikely transition from payments to an operating system

Basics of payments & Shift4

The digital dilemma of merchants

Growth engine

The misunderstood capital allocation strategy

Valuation

1. Fundamentals of Payments: A Chain Reaction

To comprehend Shift4, one must grasp the intricate dance of transactions. When a customer swipes their card, the payment processor (Shift4) acts as the intermediary, shuttling information to payment networks (e.g., Visa, Mastercard), which, in turn, interact with the issuing bank. The beauty for a merchant, is only dealing with Shift4.

2) The digital dilemma of merchants: SHIFT4´s solution

Merchants face a digital dilemma—juggling multiple solutions for POS, online orders, bookings, staff management etc. The resultant chaos of varied hardware, software, and payment solutions needed in modern commercecreates inefficiencies and headaches, which I experienced myself working at a restaurant this year. The training required for employees to learn new solutions, combined with the challenges of creating in-house solutions give these vendors switching costs. Potentially, only breach-able if one vendor manages to solve multiple others (…).

Shift4 steps in with a compelling solution: a unified merchant experience. Their payment processing technology is capable of seamlessly handling all the diverse functions a merchant may need. By offering this integrated solution, Shift4 slashes the total cost of ownership for merchants, replacing the need for multiple vendors. As an enticing sweetener to attract new merchants, they provide free hardware, to secure high-margin recurring revenue and fostering switching costs. The strategic vertical integration also opens new revenue streams, such as ticketing for stadiums.

3) Growth Engine: Firing on all cylinders

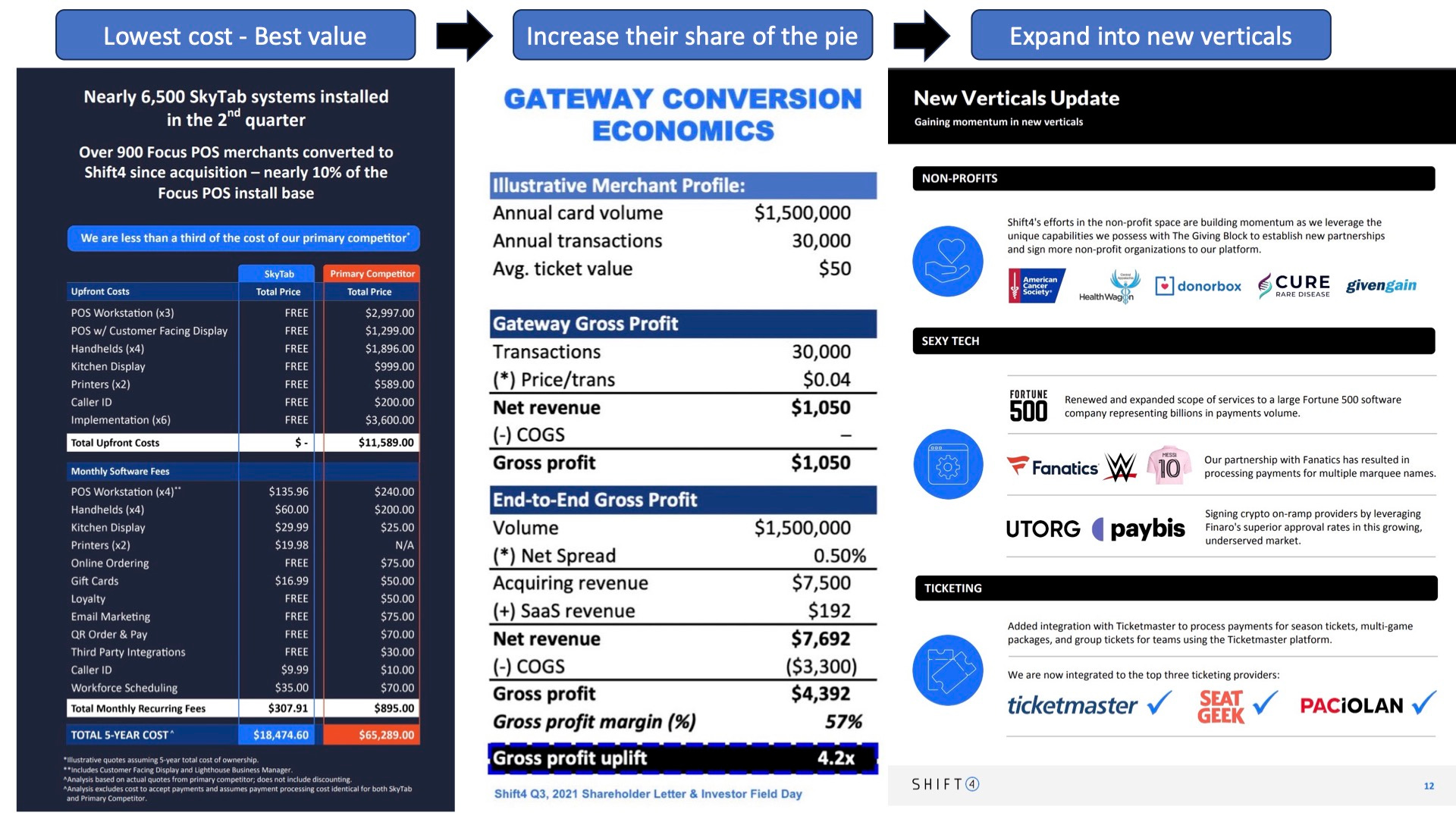

Gateway conversion economics: The shift from transaction-based fees to a percentage of payment volume improves unit economics (image above).

We derive the majority of our revenue from fees paid by our merchants, which principally include a processing fee that is charged as a percentage of end-to-end payment volume or as a fee per transaction (10K, 2022)

Deepening Merchant Relationships: By solving more merchant problems, Shift4 taps into additional subscription and payment opportunities.

Market Share Expansion: Offering the lowest cost of ownership and comprehensive capabilities, Shift4 aims to capture more market share.

Low Barriers to Entry: Providing free hardware facilitates easy entry for merchants.

Global Expansion: With the Finaro acquisition approved, Shift4 is set to go global, aided by collaboration with already global companies, such as SpaceX, PGA tours & Hilton hotels.

4) The misunderstood capital allocation strategy

Shift4 often faces criticism for its numerous post-IPO acquisitions, but it's not a random spree. Jared Isaacman, the founder with soon a quarter-century of leadership, explains the well-thought-out strategy behind Shift4's acquisitions:

I believe we are one of the best capital allocators in the industry, despite understandable skepticism regarding M&A in general. Our track record is really unmatched over the last decade. We have a playbook and it isn’t complicated: we identify differentiated technology assets with an embedded, under-monetized, payments opportunity. For the most part, we acquire these overlooked assets to support existing verticals, but at times it will take us in to new geographies or new markets. Not only has our strategy afforded us the ability to offer merchants a value proposition previously unavailable in the market, it has also resulted in our growth consistently exceeding industry averages.

The recent $100 million acquisition of Appetize this past quarter was classic Shift4. Despite what some of the critics may think, we can’t compel one of our biggest competitors to sell us their assets at a steep discount just to plug a quarterly hypothetical hole. In reality, we put ourselves in the optimal position to acquire an under-monetized payments opportunity at a very attractive price point, and in doing so dramatically accelerate our timeline in the sports and entertainment vertical by instantly adding 600+ venues to our customer base. We are in the early days of capturing ticketing volume and now have more than tripled our market share across major league sports, theme parks and well-known marquee venues. Our Appetize base case will have us exiting 2024 with $15 million of Adjusted EBITDA and years of additional opportunities to pursue. This is consistent with our general M&A criteria to be deleveraging inside of 24 months.

The Shift4 Playbook to unlock sustained value over time:

Strategic Asset Acquisition: The primary objective is to procure companies with a significant merchant base—an asset that aligns with Shift4's long-term goals.

Integration: The acquired merchant base is seamlessly woven into Shift4's payment processing ecosystem, fostering a unified and efficient experience.

Vertical Integration: Over time, Shift4 strategically guides customers to expand their usage across various functions, fortifying switching costs and enhancing the capacity to capture increasing value.

5. Valuation - Positioned to capitalize on growth rates

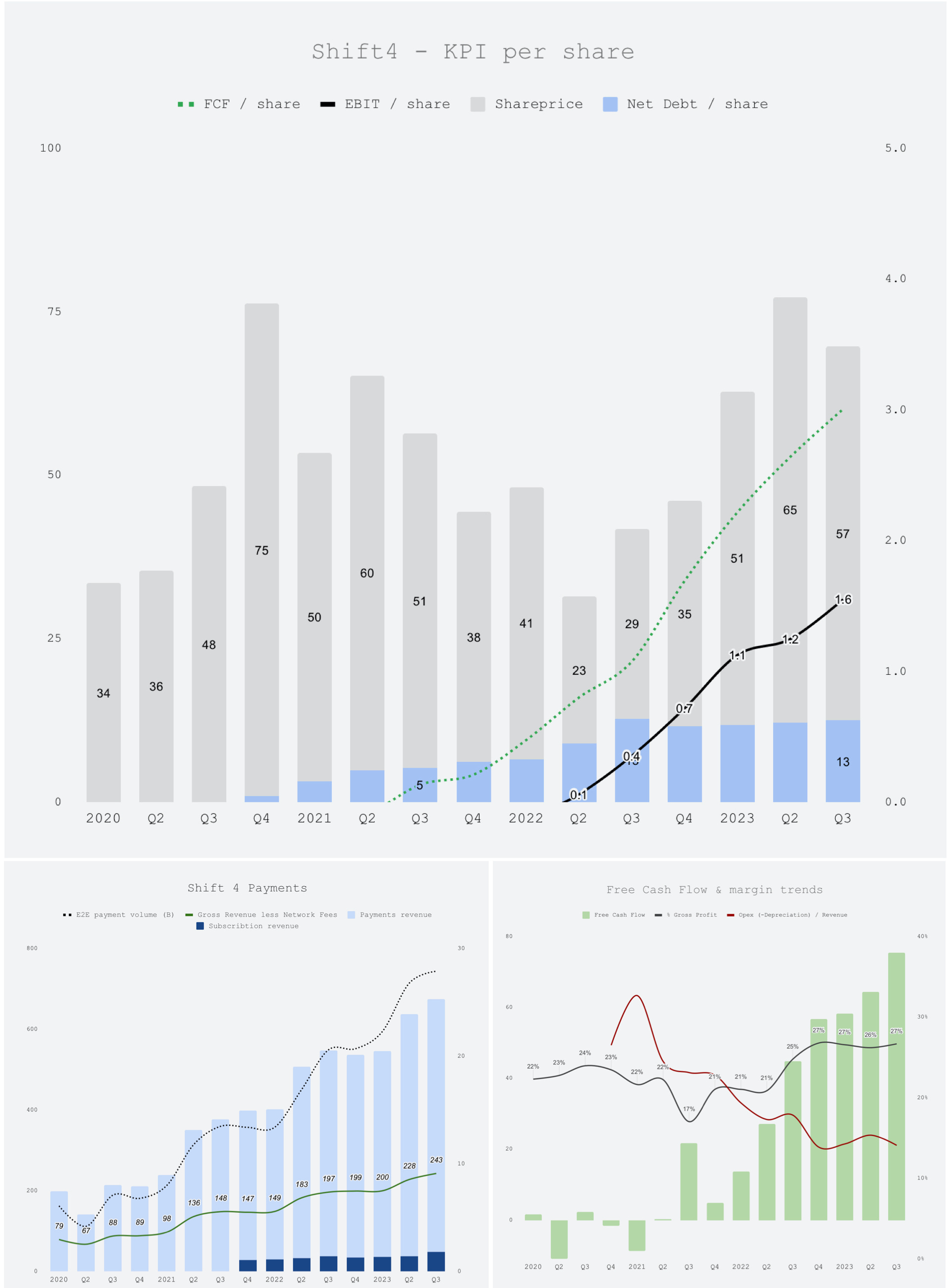

With Q3 revenues of $243 million (excluding network fees) and Q4 guidance projecting a 16% QoQ growth, including acquisitions, FOUR 0.00%↑ is on a trajectory for taking market share. Annualising the Q4 guidance indicates a robust 29% revenue surge compared to the trailing 12 months. Operating leverage is also coming into play, giving substantial profit growth from a low base. The current trailing EV/FCF at 23 paints a promising picture, especially considering the company's growttes.

However, investors should keep an eye on the Net Debt (currently at $13 per share) to EBITDA ratio (2.8). However, the debt's average rate of 1.35%, coupled with no maturities until late 2025, tempers concerns about its current height. In essence, Shift4's valuation appears not just competitive but positioned to capitalize on the company's impressive growth potential.

Hopefully, the next update on FOUR 0.00%↑ will include updates on the international expansion, but until then, I'd like to leave you with a quote from the founder himself this quarter:

I will acknowledge the market has not been kind to many in the fintech universe, but at times it does feel like we are running hard and performing well, but the crowd cheering for us to trip & fall is louder than those rooting for our success. This is what we signed up for when ringing the NYSE bell, and we will never stop fighting to exceed expectations

thanks for your post on FOUR.

Do you have any summations of current M&As of FOUR and the capital allocation ability of the company? I'm tracking those nowadays but want to hear from you.

Jared is an intelligent fanatic! This is one for the ages. I am expecting a larger player like Fiserv to make an acquisition offer considering Four's entrenched customers in the restaurant and entertainment domain.