Eurofins Scientific

36,000% return over 25 years, then flat for the last 3. Could now be a good time to look at this compounder?

Disclaimer: This newsletter is provided for informational and educational purposes only. The analysis shared is based on my personal research and is not tailored to individual circumstances. The views expressed are my own and do not constitute financial advice or recommendations to buy or sell any securities.

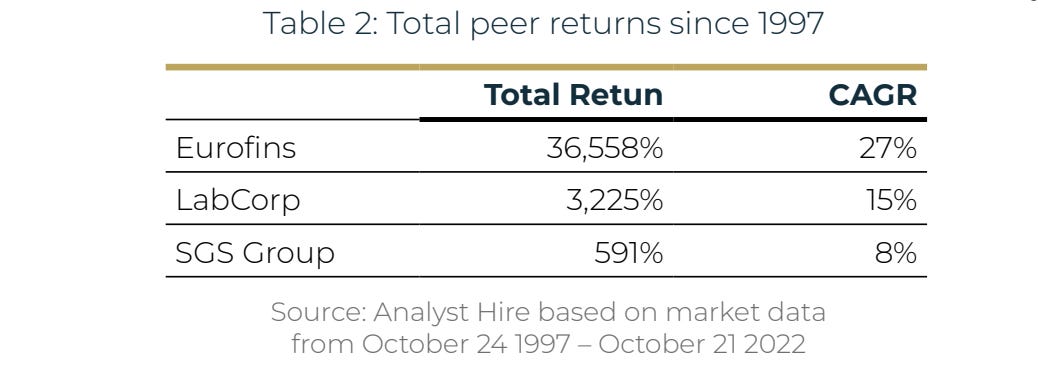

Eurofins is one of Europe’s great under-the-radar success stories, compounding at 27% annually from 1997 to 2022, turning €1 into €361. They even kept pace with the most famed compounding stories like Apple, Monster Beverages and Amazon.

Yet in the past three years, the stock has stood still. Has this compounder run out of fuel, or is this setting up an attractive entry point into a world-class business?

We believe it’s always worth asking where returns came from.

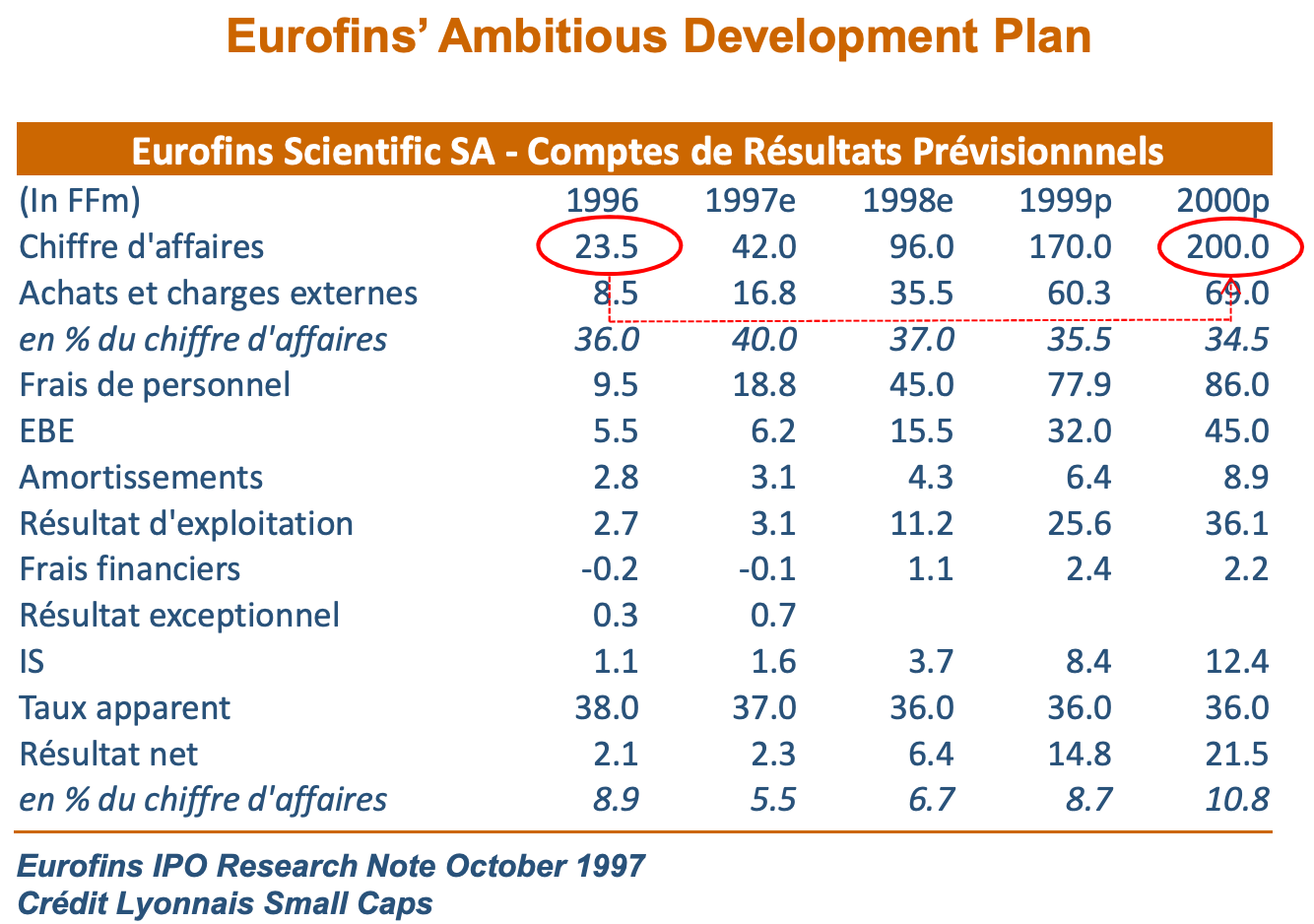

When Eurofins went public in 1997, expectations where optimistic. The company had €23.5 million in revenue, €5.5 million in EBITDA, and an enterprise value of €132 million, an expensive 24x EV/EBITDA at a time when the US 10-year yielded ~7%. Investors were paying up for growth, and Crédit Lyonnais’ research note made that clear: it projected revenues would grow almost 10x in just four years.

Chris Mayer pointed out in his studies of 100-baggers, that such compounding stories typically benefit from twin engines — the combination of growth + margin or multiple expansion. Eurofins, however, already had expectations for EBITDA margins around 17% before year 2000 (not to far off today’s 21%) and multiples have actually compressed from 24x to 9x. What explains Eurofins’ run?

Exponential Revenue growth

Revenues compounded from €23.5 million in 1996 to about €7 billion in 2024, an astonishing 23% per year for nearly three decades. That kind of growth will not repeat. But the story today can still be interesting. At ~9x EV/EBITDA, expectations have reset. Management guides for mid-single-digit organic growth, complemented by steady tuck-in acquisitions — a playbook not unlike Alimentation Couche-Tard’s.

The difference now lies in price. When you pay less for each stream of cash flow, the composition of returns shifts. Cash distributions, dividends and buybacks, become a more meaningful driver of value creation than topline growth alone. At current levels, Eurofins trades at roughly 13x distributable cash flow, or a 7–8% free cashflow yield. For patient investors, if half of that can be returned to shareholders and half reinvested into growth, starting returns can already be ok, especially when factoring in the potential of those growth investments, a topic we will come back to.

First, let’s understand the basics of their Business Model.

The Business Model

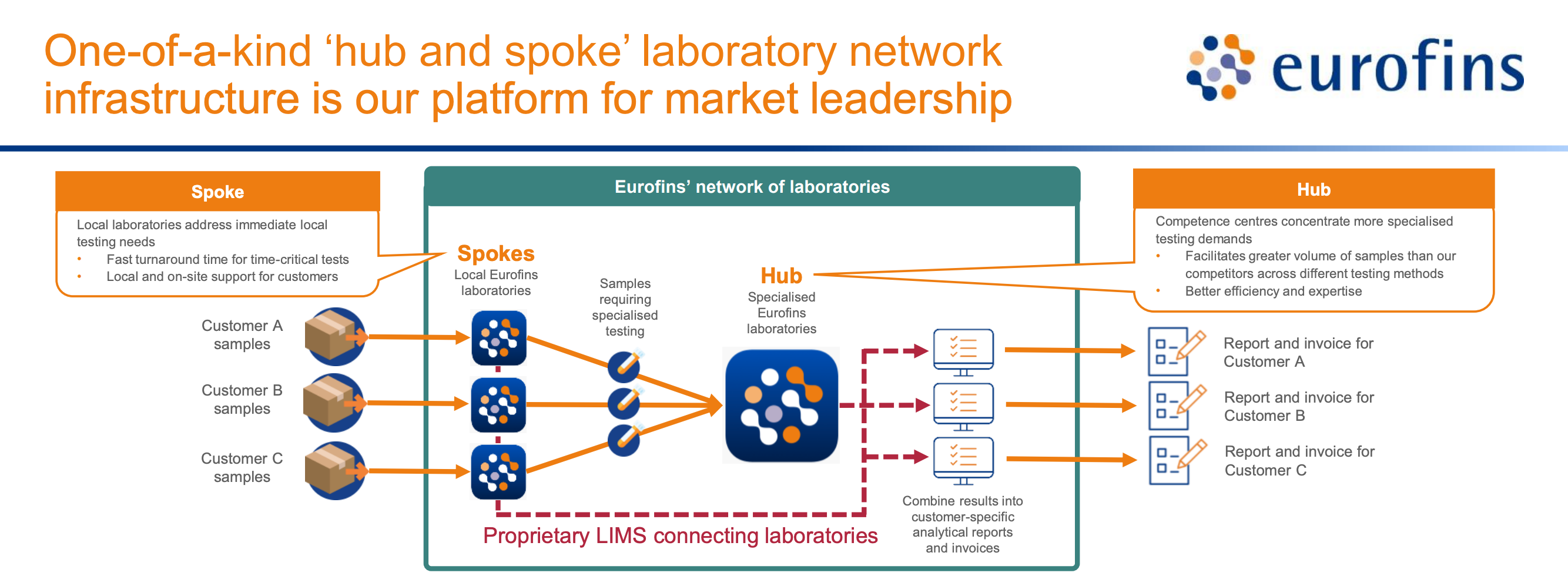

Eurofins tests to ensure products are safe, authentic, and compliant through a global network of 950 entrepreneur-led laboratories. The founder, Dr. Gilles Martin, is still the CEO and owns 35% of the company through his family holding company.

Its hub-and-spoke structure combines local customer reach with centralized scale and specialization across more than 200,000 analytical methods, where these hubs can collect samples from the spoke (local labs) for specialized testing. This model makes sense when we understand the unit economics behind running a laboratory.

A laboratory, is in effect a fixed cost, due to the facilities, equipment and staff required. Tests usually have low variable costs. Consequently, maximizing volumes and revenues (…) generate better economic returns. (Analyst Hire Report)

At its core, Eurofins’ outsized success has been driven by one thing in particular: fast turnaround times (TAT). But Eurofins’ competitive advantage extends beyond speed. It is broad and built over decades. Here are a few examples that come to mind.

1. Scale Advantage. In testing, volume matters. Eurofins’ network across 60 countries and 200,000 testing methods allow it to become a one-stop shop for many clients, while spreading fixed costs across an enormous base of samples.

2. Regulatory Barriers. Testing is highly regulated, and approvals are both costly and time-consuming. Eurofins has accumulated the certifications and trust that new entrants struggle to replicate.

3. Customer Stickiness. Once a client, Eurofins can be hard to replace. Food, pharma, water, and environmental clients rely on recurring tests, where switching risks compliance failures, delays, or worse. In a few places, labs are even physically co-located close to major producers, making Eurofins part of their daily operations.

4. Data Advantage. Decades of test results give Eurofins a proprietary knowledge base that strengthens accuracy, benchmarking, and insights. In an era of machine learning and AI-driven analysis, this dataset becomes increasingly valuable in sending back acurate and quick results.

Nevertheless, we belive Eurofins has a perhaps even more interesting edge, beyond their daily operations — being a disciplined allocator of capital.

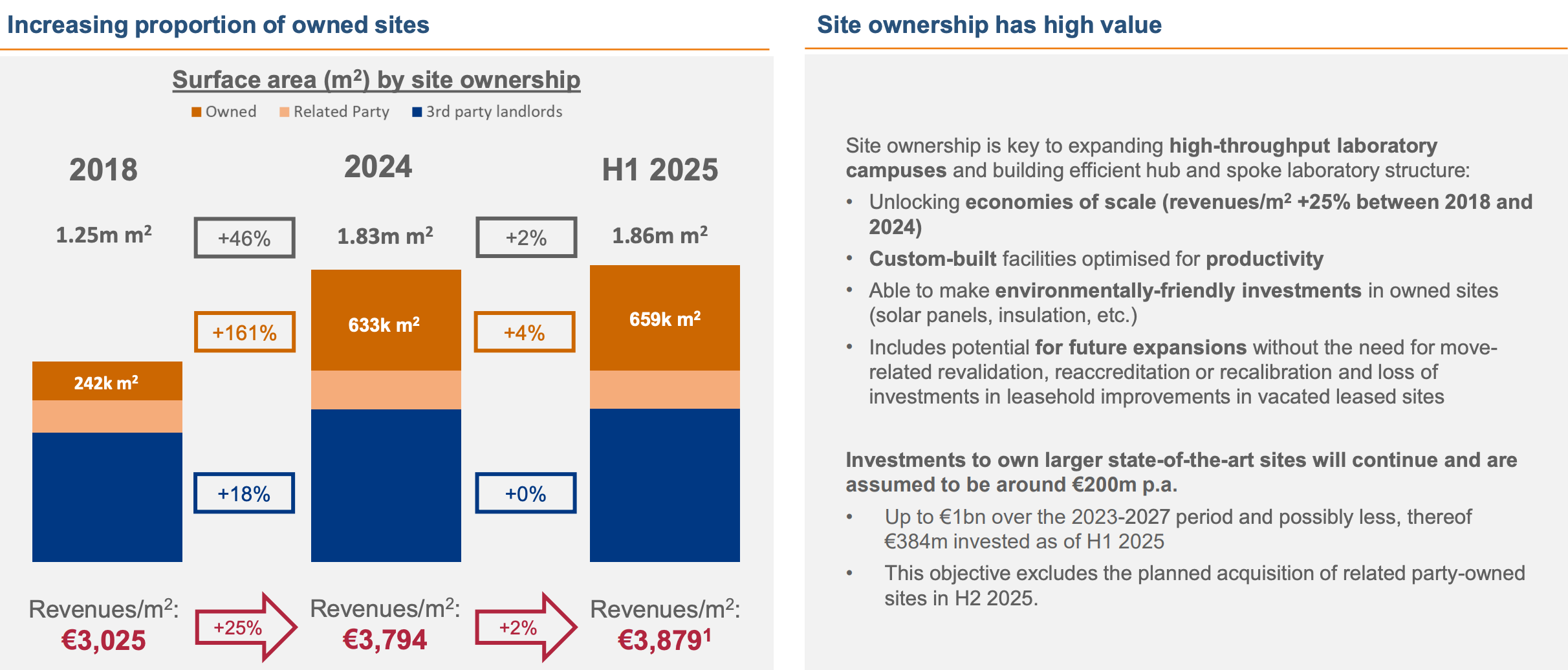

One example, is their decision to acquire key laboratory real estate now. Real estate on its own rarely delivers great returns, but here it serves a different purpose: it removes a structural vulnerability. Typically, the investments in a lab can be more costly than the building itself. Thus, some landlords have exploited this switching cost with steep rent increases, most notably in the UK.

In our view, such moves highlights the long-term thinking by management. A similar company under Private Equity ownership, would perhaps opted to do the opposite, becoming more capital-light. But we believe such bets improves the MOAT of Eurofins, and as we’ll come back to, done at a time when office real estate is not in high demand, illustrating their counter-cyclical view on capital allocation.

Capital Allocation

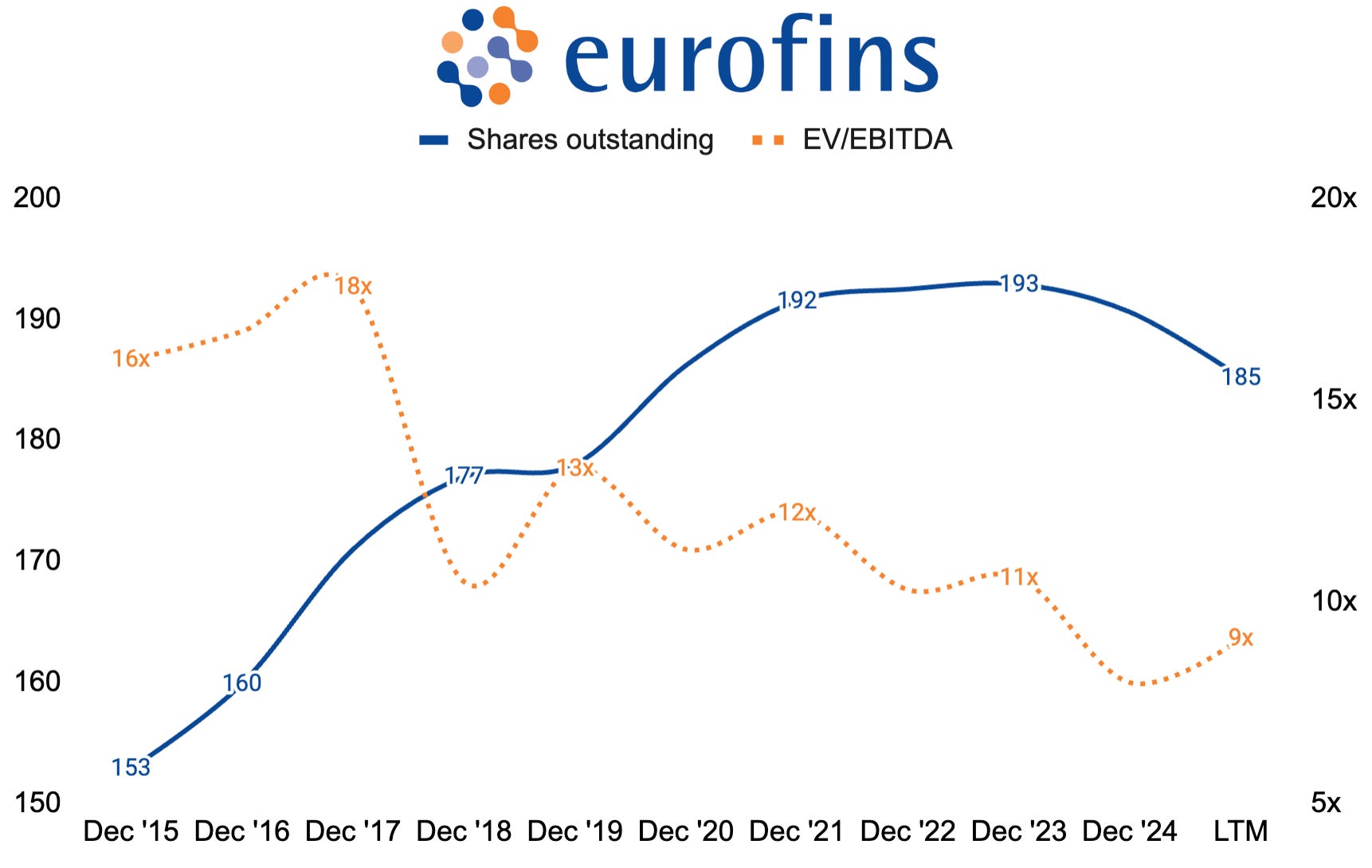

In The Outsiders, William Thorndike highlights Henry Singleton, a legendary CEO renowned for his exceptional capital allocation. Singleton was a master of counter-cyclical capital allocation: he issued shares to fund acquisitions when his stock was expensive and repurchased aggressively when it was undervalued.

Exhibit III below, shows how Eurofins mirrors this strategy, issuing shares when their stock is expensive, and like today, repurchasing shares aggressively when cheap.

However, issuing or repurchasing shares is just the icing on the cake of capital allocation — the real question should always be: where can the next euro be deployed for the highest return?

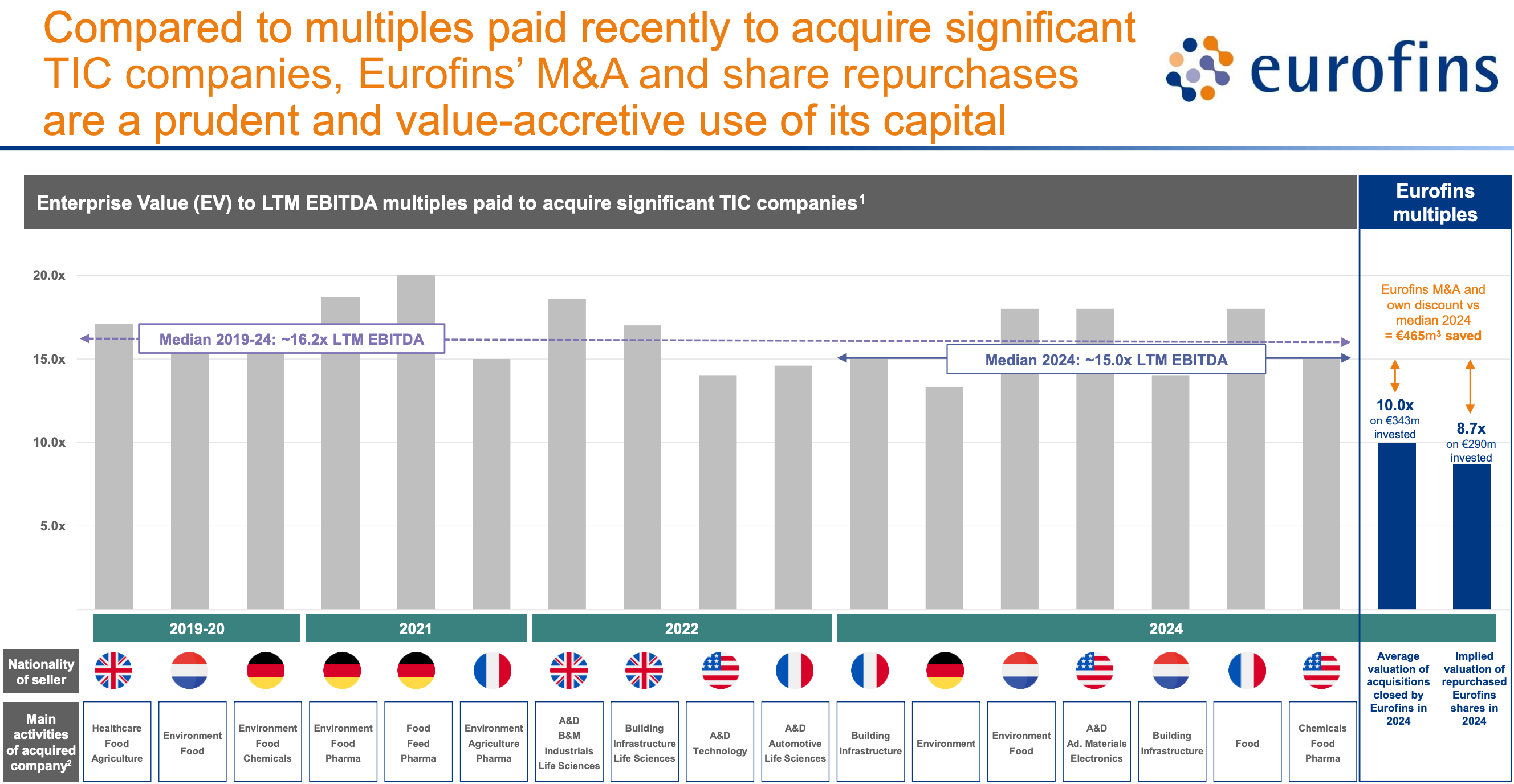

Eurofins illustrates this mindset in Exhibit IV below.

In 2024, the company repurchased its own shares at lower multiples than those paid for acquisitions — showcasing a disciplined, returns-oriented approach to capital allocation. Conversely, when shares were issued in earlier years, it was done at multiples much higher than what the company could achieve via tuck-in acquisitions. Multiple arbitrage done at its best.

While we generally dislike dilution, it can be accretive to shareholders when executed intelligently to drive per-share growth in distributable cash flows. It’s all about playing well with the hands you’re dealt with at any given time.

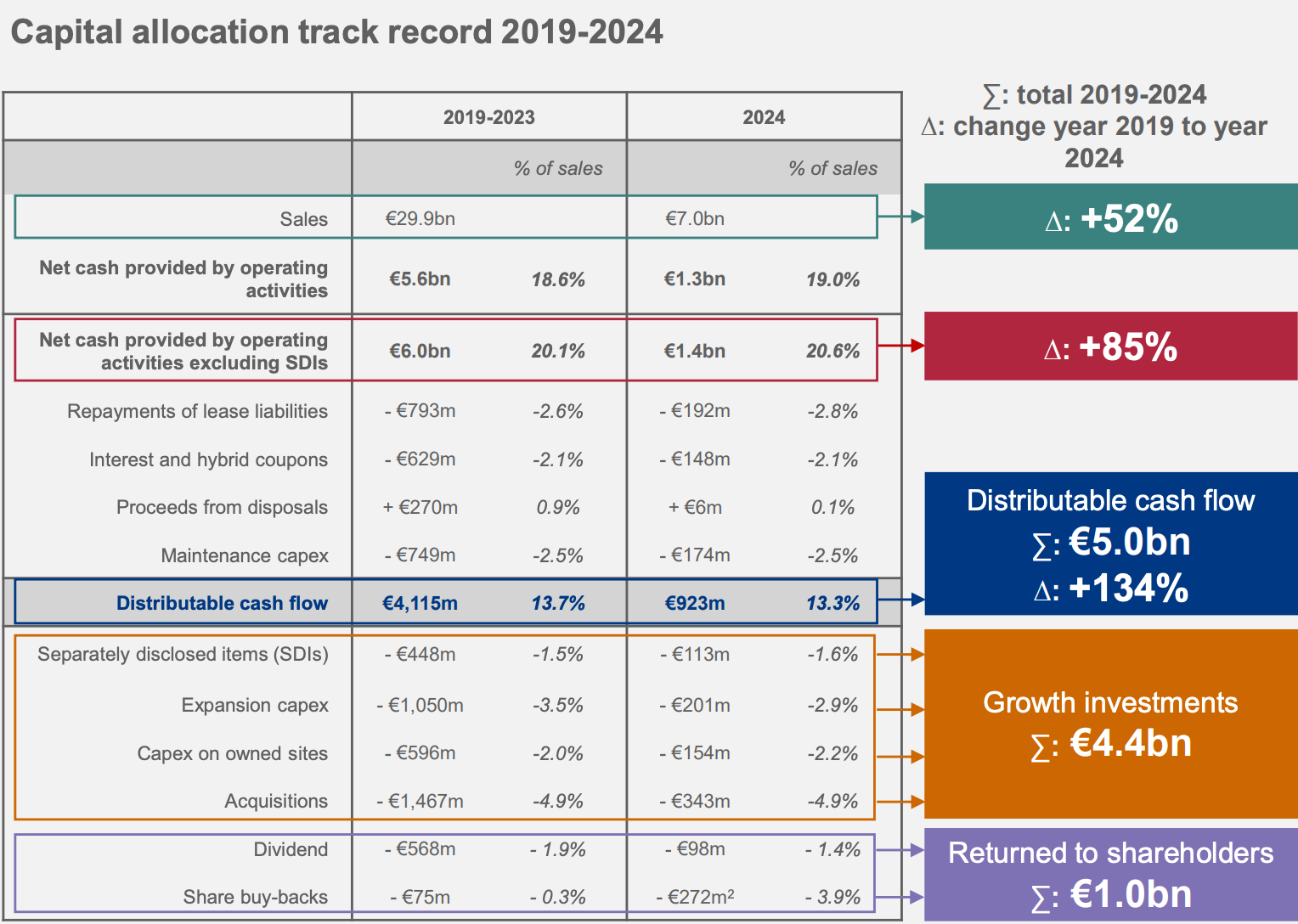

Distributable Cashflows (our favourite metric)

After deducting maintenance investments from operating cashflow, we arrive at Distributable Cash Flows, the capital that could be returned to shareholders.

In reality, Eurofins rather invest a portion of this distributable cashflow into future growth, whether through expanding operations, acquiring new sites, or making acquisitions, while also returning some cash directly to shareholders. Growth investments are highlighted in orange below. Exhibit V below, highlights where their capital has been allocated in recent years.

Eurofins’ breakdown here aligns well with how we prefer to evaluate companies — tracking growth in Distributable Cashflows and assessing how skillfully management deploys Growth Investments to generate long-term value.

And, importantly, we can measure how good they are at this.

Return on Incremental Investments (cash ROIIC)

Our preferred metric here is incremental cash-on-cash returns: Operating Cashflow grew from €540 million in 2018 to €1.4 billion in 2024. Roughly €0.9 billion in incremental cashflows. Against €4.4 billion in Growth Investments and €1.9 billion in leases and Maintenance Investments etc, this implies an incremental cash-on-cash return around 14% on incremental capital.

This is especially impressive given the significant capex tied to owning more of their sites. More specifically, they increased square footage from 240,000 → 633,000 m² over the same period (2018→2024). This means they now own 34% of their sites.

While there are businesses which boast higher ROIIC, some of which we’ve covered here before, few of those could match Eurofins’ ability to reinvest at scale. What truly matters is the combination: strong ROIIC (14%), high reinvestment rates (85%), attractive shareholder yield (~4%), and the durability of value creation, well above the cost of capital.

And of course, price matters. With a high ROIIC, companies can both grow quickly and distribute cashflows to owners, as growth consumes little incremental capital.

While different, another interesting dynamic is what happens once a company trades at a high free cashflow yield. Now, shareholders don’t require as much growth to earn decent returns themselves, more of their returns can come from dividends and buybacks.

The ideal would of course be to find the rare high reinvestment and ROIC companies trading at high free cashflow yields.

To put the math for Eurofins in context: at a market cap of ~€11 billion, shareholders stand to earn roughly a 4-5% combined dividend and buyback yield, once real estate investments taper post-2027. Layer on management’s guidance of ~6.5% long-term organic growth, plus a couple % from further acquisitions, and you’re already looking at an implied IRR close to 14%.

Additional upside could come from start-up investments (currently depressing margins), operating leverage from reduced rent costs or startups maturing, or potential efficiency gains from IT investments. Or perhaps a multiple re-rating.

All possible levers in our view.

We will cover the risks later, which (as always) can derail any investment thesis. But first, we want to highlight Eurofins’ investments in real estate, as they underscore the company’s long-term strategic mindset.

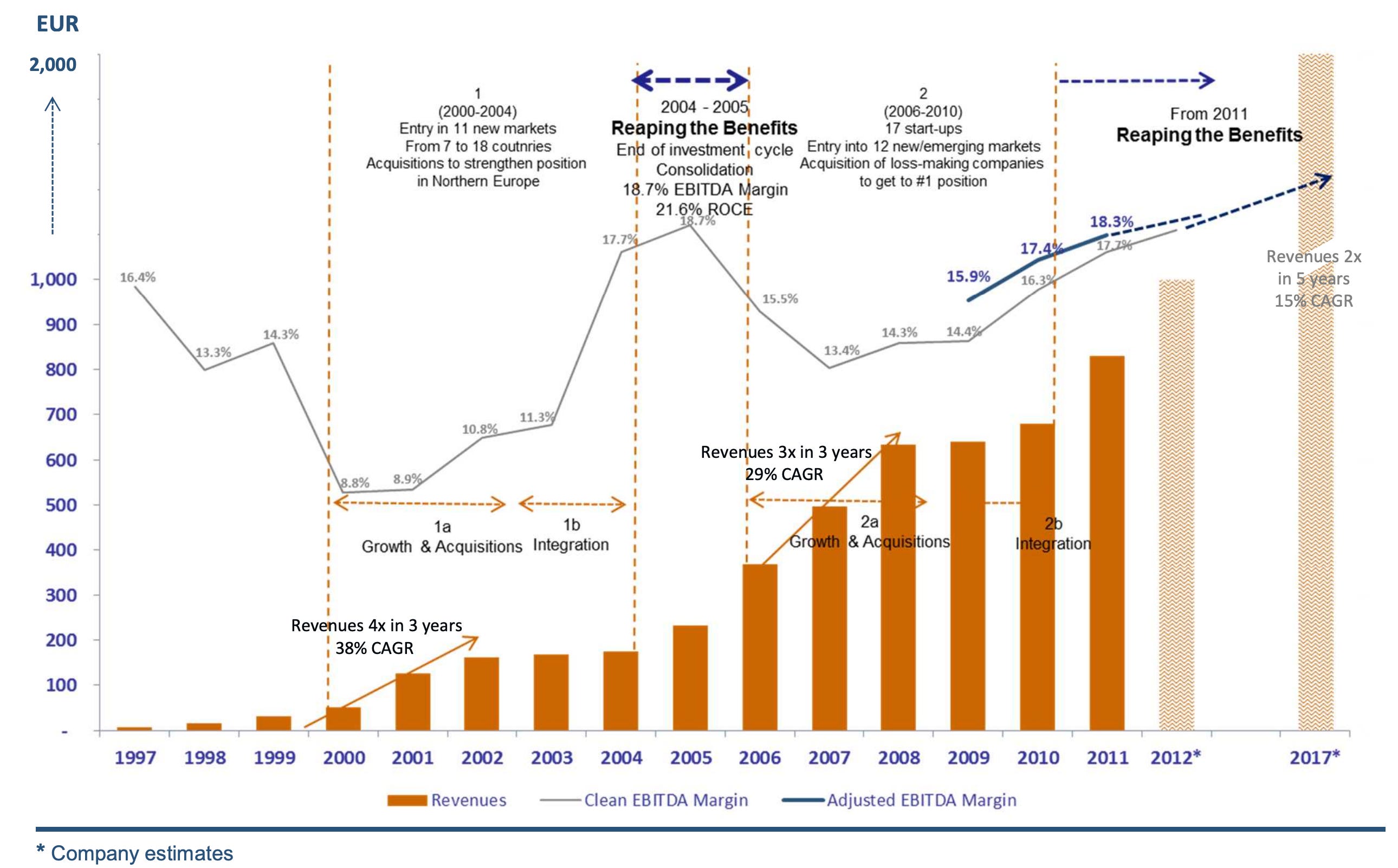

Investment Cycles & The Reverse Private Equity Playbook

Eurofins has a track record of making thoughtful, long-term bets. As illustrated in Exhibit VI below, the company has historically cycled between periods of growth and periods of harvesting those investments, with expanding profit margins.

We think this history is helpful in assessing how management think around the investments of today.

Current Investments

As seen earlier, Eurofins broke down their 2019-2024 growth investments as such:

- Acquistions (34%) - mainly tuck-in acquisitions

- Expansion capex (25%) - stuff like IT investments & lab expansions

- Capex owned sites (15%) - buying out previously leased key locations real estate

- Seperately disclosed (11%) - mainly related to start-ups investments

In total, an 85% Reinvestment Rate of distributable cashflows, with the last 15% being returned to shareholders. However, with the multiples of their own shareprice, this dynamic changed in 2024, with a third of cashflows being allocated to buybacks, showing management is ready to act once they see good opportunity.

Let’s break down the 5-year accumulated investments in a bit more detail.

Acquisitions (34% of 2024 growth capital)

Eurofins added 22 acquisitions in H1 2025, bringing the all-time total to 589. This years deals have brought in €210m in annual revenue for a cost of €150m — about 0.75x sales. On price paid, we only found multiples paid for 2024 acquisitions, of around 10x EV/EBITDA. At this price, great returns would require synergies, improved margins, or decent growth to deliver double-digit returns on capital.

Napkin Math: If new labs convert 60–70% of EBITDA into free cash flow, Eurofins locks in a ~6-7% cash yield on day one from 10x EBITDA multiple. Add 5-6% annual profit growth including synergies (similar to Eurofins organic growth targets), and returns climb toward 12%. Solid, but not spectacular. At 10x EV/EBITDA, acquisitions look fair, though not as compelling as buying back their stock at 9x. If larger synergies or growth is achieved, the return profile improves.

Our take is that acquisitions is a decent use of capital, especially with the amount Eurofins have shown they can deploy. Still, the year 1 ROIC is much lower than what we’ve found among the best serial acquirers (Momentum Group, Lifco, Topicus etc).

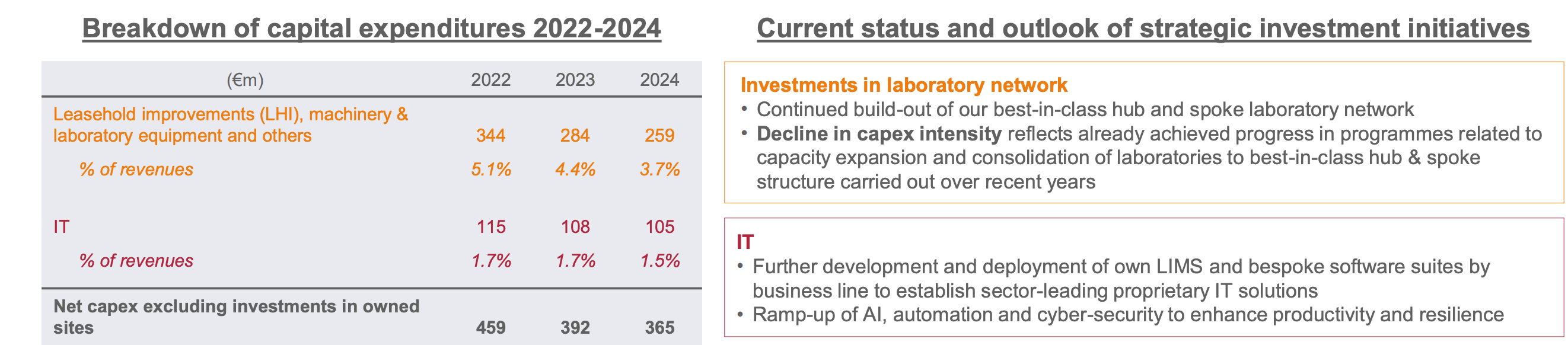

Expansion Capex (25% of growth capital)

Running a lab isn’t cheap. However, management expect declining capex intensity following their recent investments in consolidating into the hub & spoke network. This is a key reason to why management expects ROCE to expand over the next years.

This reduced capex intensity a critical piece of our Eurofins investment thesis. Current investments consume capital today, but can generate returns in many years down the line. To us, this seems like just another investment cycle, where they can now reap the benefits. When we assess the company having generated a 14% ROIIC in recent years, this includes several investments not yet having reaped all their potential. Thus, as capex intensity reduces, ROIIC should climb, all else equal.

IT Investments, on the other hand, is likely to persist at high levels, especially with the potential automation and AI can have within their labs. To illustrate the potential, management showcased an improved Asbestos Testing Flow in a 2023 presentation. Here, they highlighted how Automation and AI implementation in the Asbestos workflow, could enable 2 employees to do the previous job of 3. Automated handling, AI detection and assisted preperation, where seen as tasks robots or machines could assist more with.

Further, management called out potential competetive advantages in deploying such technologies, from: 1) Testing volumes, 2) Standardized shared practises across network, 3) Large databases to train AI and 4) Capacity to invest in technology.

We think IT investments is a necessary and great use of capital for Eurofins, because their decentralized network of labs means they can do experiments at scale, and then share best practises. Their centralized hubs for large-scale specialized testing, also have the volumes to invest in expensive technology.

On the flipside, competitors are probably also considering ways to implement such technologies, and with this still being early days, we think its difficult to suggest advancements in AI technology is a net positive to Eurofins. Another option, is that it enables more advancements in remote testing, outside Eurofins’ Laboratories.

Capex Owned Sites (15%)

For H2 2025, management called out €443 million worth of real estate they plan to buy. For these assets, Eurofins currently pays €36 million in annualized rent at these sites, almost an 8% yield in saved costs. Appraisal from independent real estate professionals confirms the attractive valuation, with equivalent reconstruction up towards €1 billion.

However, such investments ties up a lot of capital, which makes management willing to increase their leverage ratio, in order to do so. They expect these investments in H2 2025 to result in an increase of 0,2x effect on Net Debt to EBITDA.

We were surprised seeing how high the rent savings where in relations to price paid (yield). Thus, we align with management that this is a good use of capital now. Owning key real estate is an advantage which could compound over time. And being able to pull this lever at a time when office real estate etc. are unpopular, seems like the typical move a counter-cyclical capital allocator would do.

Eurofins themselves, calls out that owning these assets themselves, enables more flexibility around future-proofing buildings (energy efficiency) and custom-building them for optimised productivity (optimizing layouts). Interestingly, Eurofins have been able to improve revenues per squaremeter by roughly 27% since 2018.

Seperately Disclosed Items (11%)

Usually, we save the best for last, and we found start-ups as a very interesting capital deployment opportunity for Eurofins. It’s easy to imagine Eurofins as just a bunch of decentralized old labs within a massive network. But reality is much more nuanced.

Eurofins have initiated 325 start-ups and 118 Blood-collection points (BCS) since year 2000. The strategic rational has typically been as a complement to their acquisition strategy, typically in high-growth markets without availability or affordable acquisition targets. Importantly, returns on these investments are showing excellent results.

In 2024, mature start-ups from the period 2010 - 2021, generated a 59% ROCE. No wonder management plans to continue deploying more capital here.

That said, this is a form of organic investment where simply adding more capital may not necessarily lead to better results. Success here likely depends as much on finding and empowering the right people as it does on financial resources. Therefore, we wouldn’t expect the percentage of distributable cashflows here to increase that much.

Dividends & Buybacks

Capital distributions have become a meaningful driver of shareholder returns at today’s valuation. Subsequently, management is directing a significant share of free cash flow toward buybacks, alongside the steady dividend.

With investments in owned lab sites tapering off, most key locations soon secured, we expect more excess cash to be available for distribution (or growth) in the years ahead. You’ll find more of this in the Valuation section, but first let’s look at risks.

BUSINESS RISKS

Assessing risks are hard. The future is inherently uncertain, but what can we learn from its past? With this in mind, we tried collecting what risks in their annual reports have actually materialized in the last decade using AI tools. After each point, we cover our own thoughts in this particular subject.

Last Decade’s risks materializing

Cybersecurity and Operational Disruption Risk

In 2019, Eurofins subsidiary NPCC experienced a ransomware attack, where 20,000 forensic cases in criminal investigations where delayed as a result.

In July 2025, the 2019 acquired subsidiary NMDL, experienced a serious data breach, where half a million Dutch cancer screening women’s data where stolen.

Cybersecurity is a critical business risk, both for litigations and reputation. On the other hand, one advantage of Eurofins’ decentralized structure, is that these risks typically don’t materialize groupwide. However, this decentralization can also be a two-sided sword.

For instance, smaller labs are likely to have worse IT systems, and thus may be easier targets. Even if a case like NMDL occurs within one subsidiary, the risks can be felt by the Eurofins group, also in terms of reputational damage.

Similarly, while centralizing and modernizing IT systems may reduce cybersecurity risks, they could also increase the vulnerability to group-wide outages, as perhaps one breach could reach more of the Eurofins group.

Other Reputational Risks

Eurofins was accused in a short-report by Muddy Waters in 2014. While this report seem to have weighed on the stock price ever since, a detailed forensic audit by Ernst & Young later found no evidence of misstatements or irragularities.

Short reports feel unsettling at first, but they can also offer valuable opportunities for investors.

First, if someone has put in significant effort to uncover risks, and you can build solid counterarguments, this can strengthen your conviction.

Second, once the initial turbulence subsides and you’ve analyzed the claims, the accusations may weigh more heavily on the stock price than the actual probability of them materializing. This disconnect can create good buying opportunities — both for the company through buybacks and for investors.

Acquisition Risks

With 59 acquisitions completed in 2022 for instance, this typically brings risks within integration, culture, potential management transitions and more. While we haven’t found examples of outright failures, it’s almost certain that some transactions have been less successful than others. Retaining key employees and preserving an entrepreneurial culture are particularly dependent on well-structured incentive systems, making this an interesting area for deeper research.

That said, Eurofins’ strong track record of organic growth, measured from revenue streams not acquired in the past year, suggests that integration has not created significant long-term issues. Another positive sign, is that the average cash-ROIIC for the group (14%) is much higher than that achieved in year 1 following an acquisition (10% EBITDA yield), suggesting value creation also occurs within most subsidiaries, also newly acquired ones.

Technological Risks

A risk we think a lot about, but couldn’t find much material on, is the potential of decentralized testing.

In our own full-time profession within Physiological Endurance Testing, we can see increased availability of equipment customers can use themselves, outside labs. For instance, athletes can now do hemoglobin testing themselves, without stepping into the doctor’s office at all.

Could such risks play out in some of Eurofins 200,000 testing methods as well?

We find it hard to generalize such theories. Perhaps in the less complex tests, one could imagine a cheap collector sending signals to a smartphone for further analysis, could reduce demand for laboratory testing in some verticals. However, this risk would never apply broadly across Eurofins’ 200,000 different testing methods. Highly specialized or heavily regulated testing will remain anchored in professional labs, where reliability and accuracy are hard to match.

When considering this risk, another emerges: the incentives around developing new testing methods. We appreciate Eurofins’ willingness to deploy capital into start-ups, as these players often have stronger incentives to innovate. However, cost-reducing innovations are typically easier for new entrants to pursue. This dynamic is often known as Counter-Positioning — when challengers can disrupt incumbents by offering a cheaper or better alternative without jeopardizing existing revenue streams.

The overarching potential risk here, is how Eurofins adopts to changing technology. We think its worthwhile reflecting over their decentralized structure in this regard.

Decentralization - A double-edged sword?

A positive about Decentralization, is that it can be a structure avoiding bureacracy, typically limiting the speed of which decisions is taken at large organisations. Entrepreneurial units can experiment and adopt tools and learnings faster. On the flipside, coordination can be difficult in local units that value autonomy, like implementing transformational large-scale rollouts of new technology tools etc.

Management Incentives & Valuation

Most of today’s write-up on Eurofins was free to read — only the Incentives and Valuation section is reserved for paid members. If you consider joining, a subscription is $60 per year or $8 per month.