Investor: Well-Oiled Growth Engine

Investor AB (1916), a family-run conglomerate with a 17% CAGR over the last 20 years! No wonder it´s being referred to as the Swedish Berkshire. Let´s dive into what lies beneath this giant

Mission Statement: We create value for people and society by building strong and sustainable businesses, through engaged ownership

The Engaged Owner

At the core of Investor AB is the Wallenberg Foundation, serving as the predominant owner and controlling 50% of Investor's voting rights. Established by the Wallenberg family in 1916, Investor maintains a lasting connection with the Wallenbergs, who continue to actively participate in its endeavors. The Wallenberg Foundation receives dividends from their ownership in Investor, FAM, and Navigare Investments, channeling these earnings into research grants and educational initiatives in Sweden. These initiatives span diverse fields such as healthcare, natural science, and technology—reflecting the typical industries you will find Investor companies thrive.

The Wallenberg Foundation's pivotal role as a long-term, value-driven active owner significantly contributes to Investor's commitment to societal and shareholder value creation. Notably, this relationship may provide Investor with a strategic advantage, by having direct access to a pool of talent & research insights.

The core positions

40% of Investor's total value is concentrated in three key holdings: Atlas Copco, ABB, and Mölnlycke. These companies not only represent substantial portions of Investor's portfolio but also embody a strategic focus on sectors with sustained long-term momentum. This deliberate selection underscores Investor's commitment to cultivating value through investments in industries with robust and enduring prospects. A quick dive into their margin stability, cash-conversion, return on capital and revenue growth, suggests their competitive positions within their fields is strong.

Above the surface

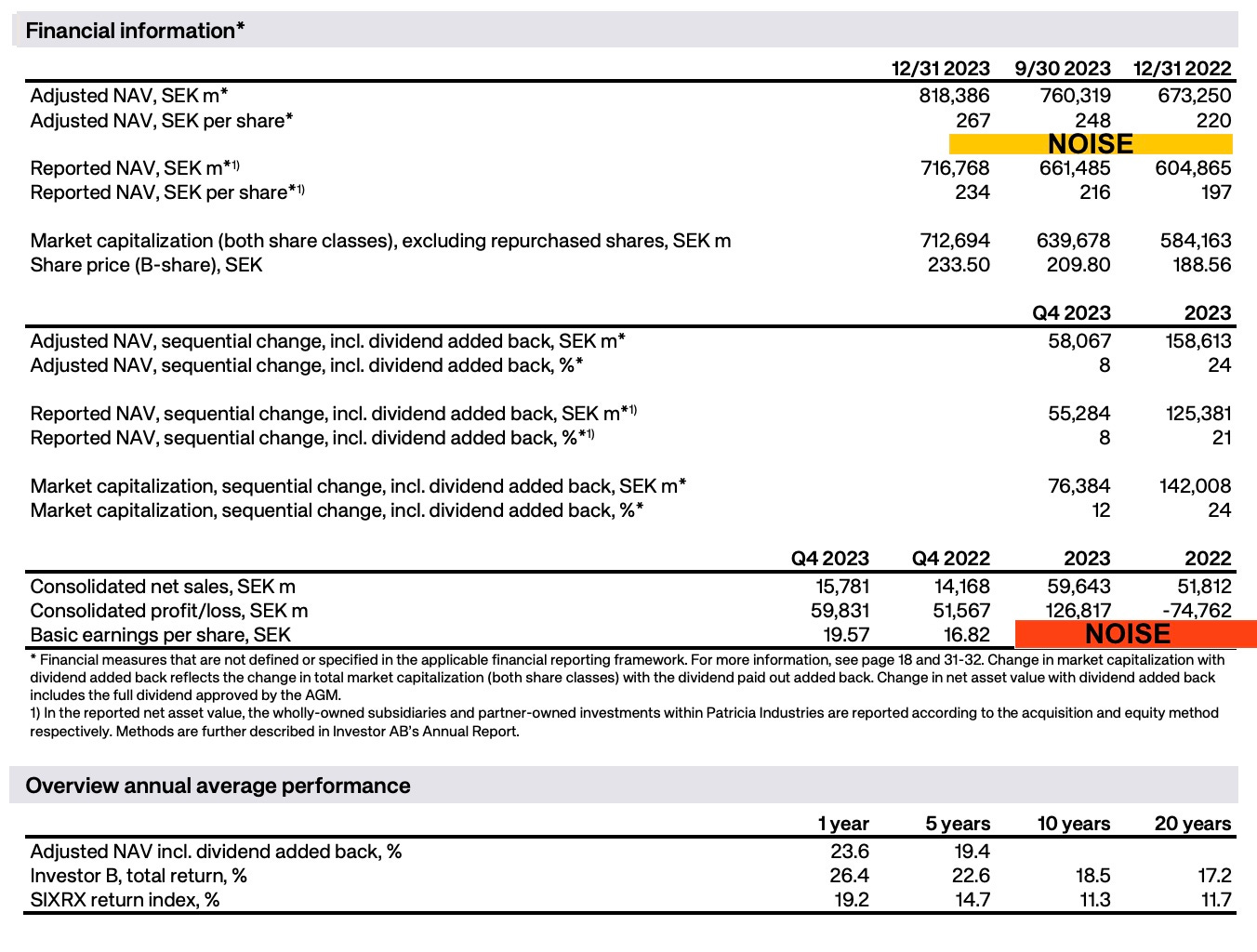

Two metrics especially stand out when you read Investor´s annual report - consolidated profits and discount to net asset value (NAV). While these metrics are often discussed, I will now lay out my case why they provide more noise than signal, and what we should study to really understand the growth in intrinsic value per share.

A holding company, like Exor, Brookfield or Investor, typically trades at a discount to it´s underlying values. This may provide investors with some “margin of safety”. However, there are no guarantee that the discount would decrease. Importantly, even if Investor´s Listed companies traded at overvalued prices, you may still be able to buy Investor at a discount to NAV - however, this does not mean you buy it at an attractive price. To reveal this, you need to understand the consolidated profits (later in article) and the future prospect/assumptions priced in. But, there is a catch. Consolidated profits reported for conglomerates also contain noise - apparent within both Berkshire & Investor´s quarterly reports. This is exemplified with Investors consolidated profits being -75B SEK in 2022 and 126B SEK in 2023 - a fluctuation primarily explained by falling stock prices in 2022 and the opposite in 2023. Remember, if you buy a stock (all else equal) after it´s share-price have fallen, risk actually decreases, with assumptions for adequate returns being lowered.

Beneath the surface

By multiplying Investors ownership stake today in Listed Companies & EQT with their respective profits, we receive consolidated profit numbers. When looking at earnings before interest & tax (EBIT), one can see a good overview of the development of the portfolio of companies. Up and to the right sums this up. In line with recent interest rate increases, the valuation (EV / EBIT) of Investor also looks to have fallen.

Cashflows & Capital Allocation

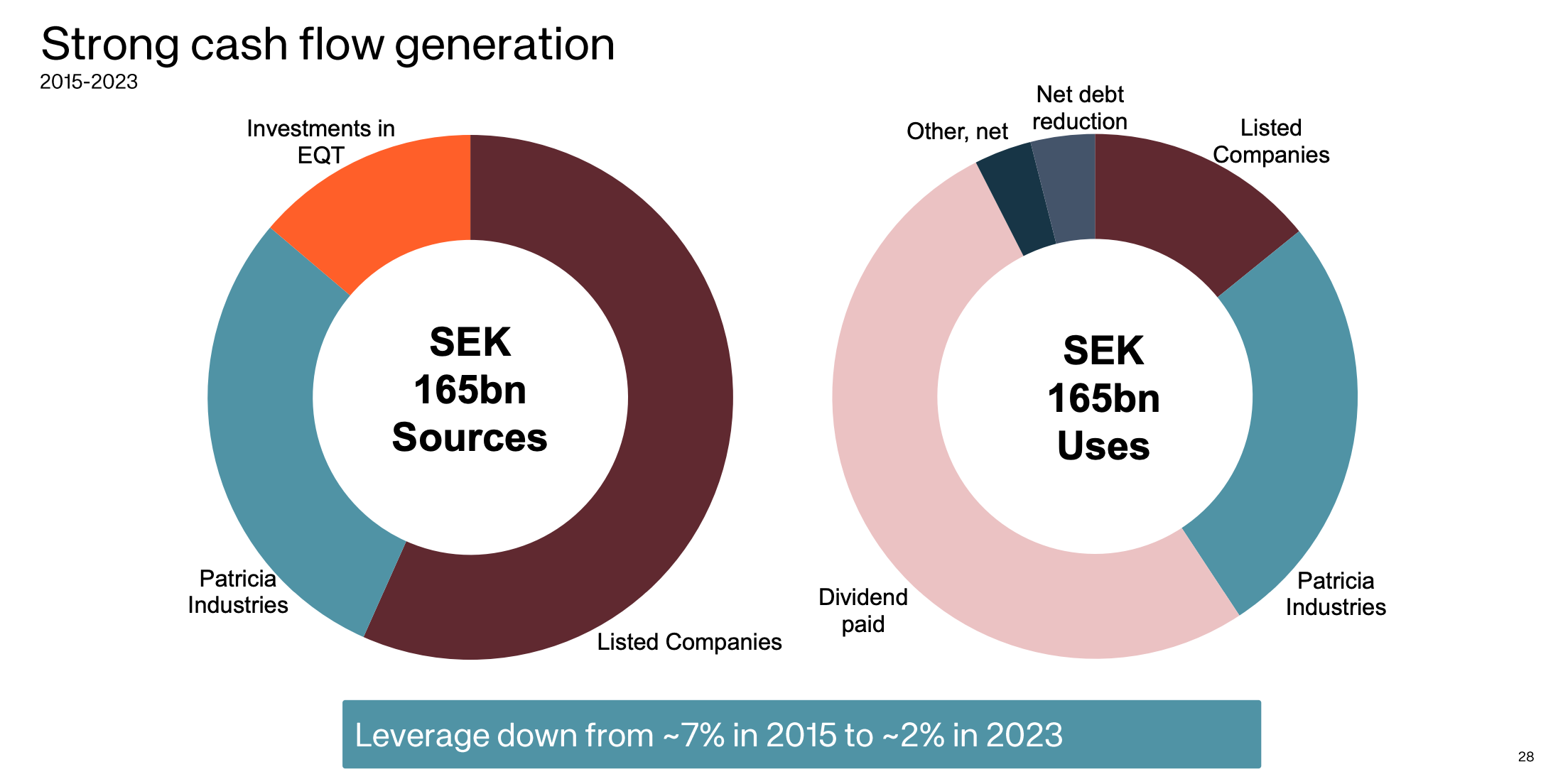

Behind conglomerates & especially serial acquirers, capital allocation may be the most important task. Of all the 165B SEK Investor have received, they have spent ~50% on paying dividends, ~30% to reinvest into Patricia, ~10% to reinvest into Listed and the rest going to strengthen the balance sheet (picture below). The decision to distribute this much capital to dividends is understandable, given the Wallenberg Foundation need for cash. In general, this slows down compounding, as dividends can be an expensive luxury for compounding - with less money to reinvest. Despite this, Investor shares have had a CAGR of 17% over the last 20 years? This is somewhat unusual for a company above 100+ years, with a 2-3% dividend yield at a payout ratio of 50%. What is the secret sauce behind Investors growth?

The Dual Reinvestment Engine

The secret sauce is that there is not one, but 2 reinvestment engines of Investor. The first being the above pie charts, and the second being the underlying cashflows not distributed as dividends. As these companies (EQT & Listed) only allocate a certain percent of profits to dividends, a significant sum of capital may be reinvested as well, without touching Investor hands. It’s like having threes outside your garden, their growth should count similarly to the ones within.

Retained earnings for Atlas Copco, SEB, Epiroc, SAAB & Sobi have grown by a 5-year CAGR of 16, 8, 15, 18 and 26%, while ABB and Astra Zeneca are ~ flat. In the same time, EPS have grown by respectively: 15, 18, 14, 14, -5, 36 and 42% CAGR!

For the largest position, Atlas Copco, “only” 1/4 of operating cashflows are paid out to shareholders (Investor), with the remaining 3/4 being used for Balance Sheet, maintenance capex and most importantly, reinvested for growth - at a 5-year average of 27% ROCE! If you take Investors 17% share of the increased equity of Atlas Copco over the last 5y, this comes out to 7B SEK (of 40B), an extra 5% of equity reinvested to the pie chart above, from one company alone.

In sum, it’s like Investor have a ~4-5% cashflow yield to allocate, but some extra percent of cash is being reinvested without touching their hands. This is the recipe for compounding 17% over the last 20 years. Even after you subtract the large >2% dividend yield, you still have an enormous reinvestment engine (arrows going back up in picture). Below you will see how much impact some extra reinvestments can make:

Future Prospects & Valuation

By being positioned in industries with secular growth (primarily healthcare & technology), INVESTOR have opportunities to capture and execute towards. With their dual focus for their 2 reinvestment engines, both as operators of Patricia Industries, and as active board members and majority shareholders in Listed Companies & EQT, they have plenty of challenges to tackle. With leverage in the lower range of their target today, there is more capital available to be reinvested than any time before. My bet is that the $80B giant will continue to compound, with diversification reducing its downside, and strong capital allocation enabling upside.

Below I present a simple hypothetical valuation box for INVE A or B shares. As always, the stock price may go way higher or way lower, but this gives some ballpark numbers to play around with. As you can see in my example, returns is mostly driven from topline growth and margin stability, not multiples increasing from their “discount to NAV. There is always the chance of spinning out Patricia, while this would probably create shareholder value, its a short term move, if you ask me. You only get the rerating once, while the beauty of compounding lies in the time it's able to do so - With Investor AB being a prime example out there of doing so for now a 108 years

Disclaimer: I do own shares of INVE A and none of this is financial advice.

Really enjoyed this analysis thanks. Looking at the directors’ holdings and around this generally, I can’t work out if A or B shares are better for a retail investor (I’m not interested in voting rights particularly). Is there a better reason to own A shares in your view? Thanks again for the article

Do you have a sum of parts analysis?