Kontron AG

Growing Order Backlog, Improved Business Quality & Price down. Opportunity?

Two weeks ago, a man accidentally gained control of 7,000 robot vacuums, including their cameras, while trying to steer his own vacuum with a gaming controller.

This was not a sophisticated cyberattack. It was weak security in connected devices. As connectivity also expands into higher-stakes industries than household appliances, security shifts from a feature to a neccesity.

This is where Kontron operates — supplying embedded systems and connectivity solutions to mission-critical infrastructure, like components used in the F-16. This writeup aims to get a sufficient understanding of the Austrian €1.4 billion firm Kontron, to see whether it can be an interesting Investment Opportunity.

Disclaimer: This newsletter is provided for informational and educational purposes only. The views expressed are my own and do not constitute financial advice or recommendations to buy or sell any securities. The author did not own shares in Kontron as of the time writing this.

Overview

We will go through these topics, starting out with a comparison to a firm we know well.

Kontron vs Norbit

Business Model & Capital Allocation

Capital Allocation & Growth Opportunity

Management & Incentives

Risks & Acquisition of Katek

Valuation

Kontron vs Norbit

Kontron reminds us a lot of Norbit. And not just because you can find some of their products in similar places. We’ll go through 5 key traits we think they have in common.

1. Niche, high-specification components

Both companies operate in technically demanding niches, supplying components where reliability is critical and failure is costly.

Technical complexity and niche end-markets acts as barriers to entry. Customers require high performance, consistent up-time, certification, security, software and long product lifecycles. It’s very different than commoditized electronics.

2. Local manufacturing and in-house R&D

While Kontron did struggle during the chip-shortage of 2022, they are still one of few European manufacturers of certain components, and with their in-house R&D department (3,600 engineers and €200 million spend), they also seem to benefit from the “Made in Europe” label helping win some contracts where that has value.

This is especially relevant in the Defence sector.

3. Having acquired 20+ companies

We’ve shared a lot of research on Serial Acquirers before. Where both Kontron and Norbit is not considered typical serial acquirers doing multiple deals per year, they are more a hybrid — both investing organically and doing 0-2 M&A deals annually.

We’ll look closer on a recent deal Kontron further down.

4. Outsider CEO’s

Both Hannes Niederhauser and Per Jørgen Weisethaunet have unusually high stock ownership relative to their salaries. Hannes was paid just €8k (!) in total remuneration in 2024, whereas Per Jørgen was closer to €690k (60% of this tied to bonuses).

Comparing this to their ownership stakes, Hannes with €73 million (5% stake) and Per Jørgen’s €131 million (11% stake), means their stock ownership stood at 9,000x and 190x their yearly compensation by the company. This is exactly the type of management alignment we’d like to see, as we know these business operators will be kept more up at night than us if a Black Swan occurs. It also signals these managers are highly incentivized to focus on the long-term success of their companies.

The outsized ownership stake relative to base salary is a sign of an Outsider CEO.

5. High Cash Conversion

A concern we had with Kontron, was not finding much disclosure of returns on capital, we think of that as a yellow flag for a (relatively) capital intensive firm like Kontron.

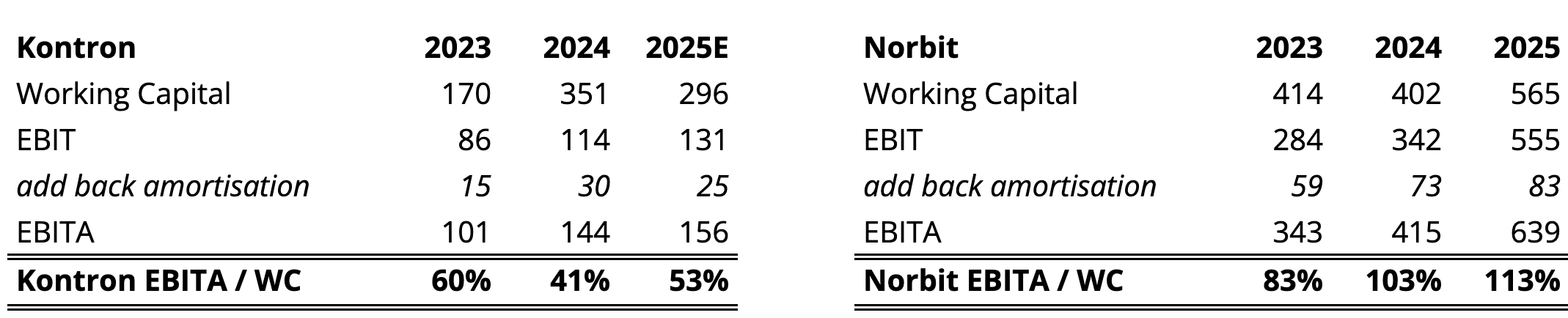

Importantly, Kontron invests heavily in both R&D, tangible capex and acquisitions. Which metric we use to measure capital efficiency matters. For instance, in our calculations, Return on Capital Employed is in the low teens, nowhere near the likes of Norbit. Another return metric we think is underappreciated, is the Bergman & Beving model, popularized by Addtech and Momentum Group, two of B&B’s spinoffs.

Momentum Group’s idea is simple: for asset-light or acquisition-driven industrials, the real capital at work often lives in working capital — receivables, inventory, and payables — rather than fixed assets. Their framework measures value creation as EBITA divided by working capital, where EBITA is EBIT plus amortization of acquired intangibles specifically. Stripping out acquired intangible amortization removes the accounting noise from M&A purchase price allocation, and better measure underlying profitability.

When we put Kontron and Norbit through this calculation, Kontron gets mid 50% and Norbit’s around 100% (!), both above the upper 45% target for the B&B group.

Importantly, Kontron management have called out that there are still room to improve the Working Capital further, especially in the newly acquired solar company Katek. You can see the big jump in working capital in 2024, most of which from that deal.

Good working capital efficiency combined with a large growth opportunity ahead tends to be a good combination for great incremental returns on capital.

Business Model & Capital Allocation

In this segment, we want to try and answer 3 questions.

Are profits defensible over time? Pace of Innovation and/or Competetive edge

Are customer demand cyclical? Are there any secular demand drivers?

Track-record of clever Capital Allocation? And are there attractive places to reinvest capital currently?

We think assessing whether price is cheap, can wait until the end. Most mediocre businesses should probably just be rented until a price discrepency narrows. That’s not our strategy, we’d rather own assets where time is our friend.

Kontron typically operates in niche markets with high barriers to entry. This is important, as larger end-markets are typically more at risk to be commoditized. The Kontron Harrakan is a good example of such a product, made for tough environments.

The competetive position of Kontron varies by vertical. Within high-speed railways for instance, Kontron has >50% market share and 25% EBITDA margins, and is the sole supplier of the new standard, FRMCS edge devices. In contrast, they have closer to 10% EBITDA margins in their automotive segment. There’s no doubt Kontron operates in a competetive field, but their decision to avoid the larger consumer electronics market is a sign they prefer to look for more technical and niche markets.

Kontron view their R&D capacity as a competetive advantage. With more than 3,000 engineers and annual R&D budgets of €200 million (14% of revenue), Kontron is an innovation force in their field. Management highlights their in-house engineering workforce as cost-competetive to, being primarily located in Central and Eastern Europe, with average salaries around €55k p.a.

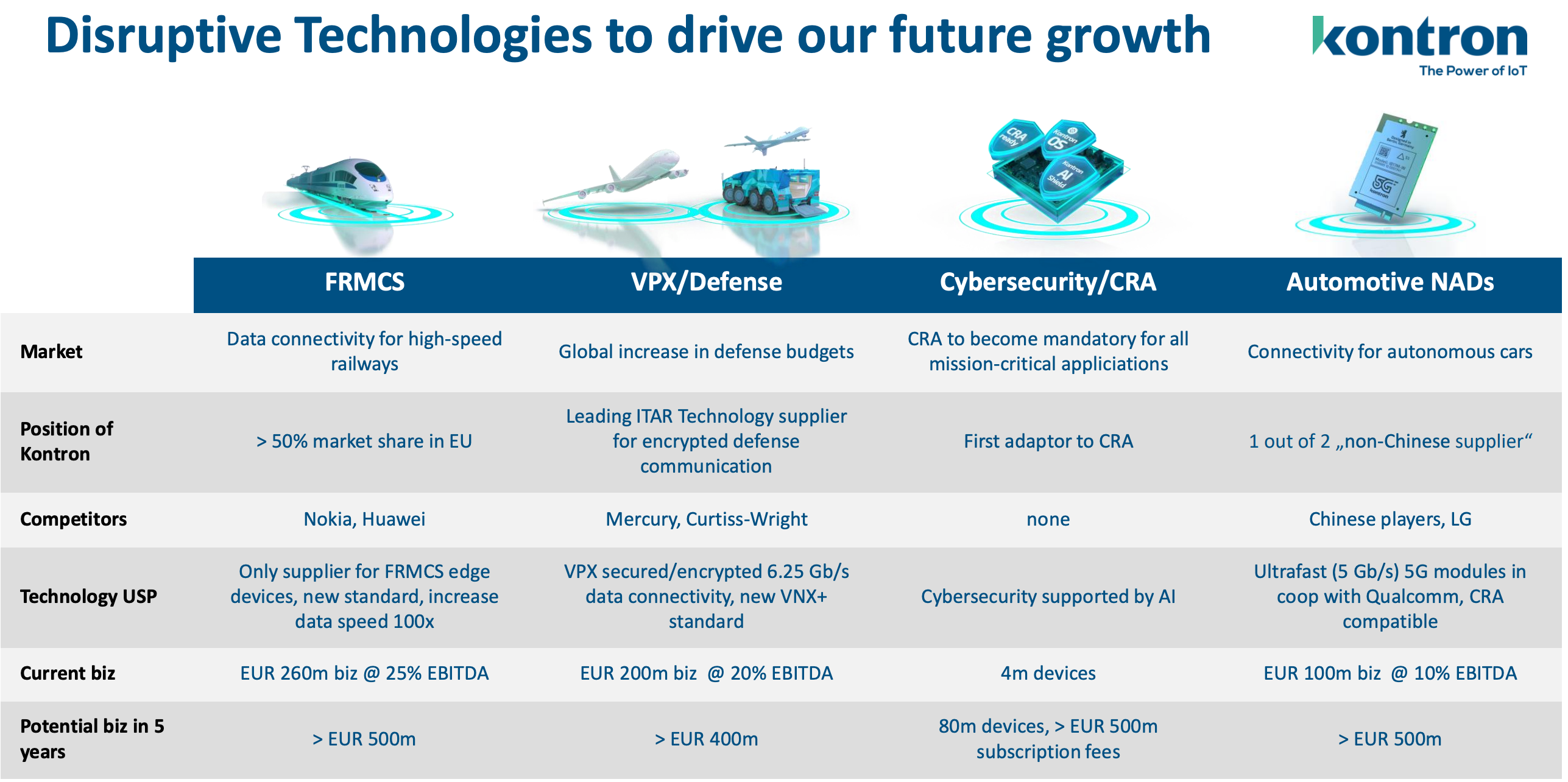

And with the evolving technology, no wonder Kontron invests so heavily in R&D. They expect disruptive technologies to drive future growth (Exhibit 3).

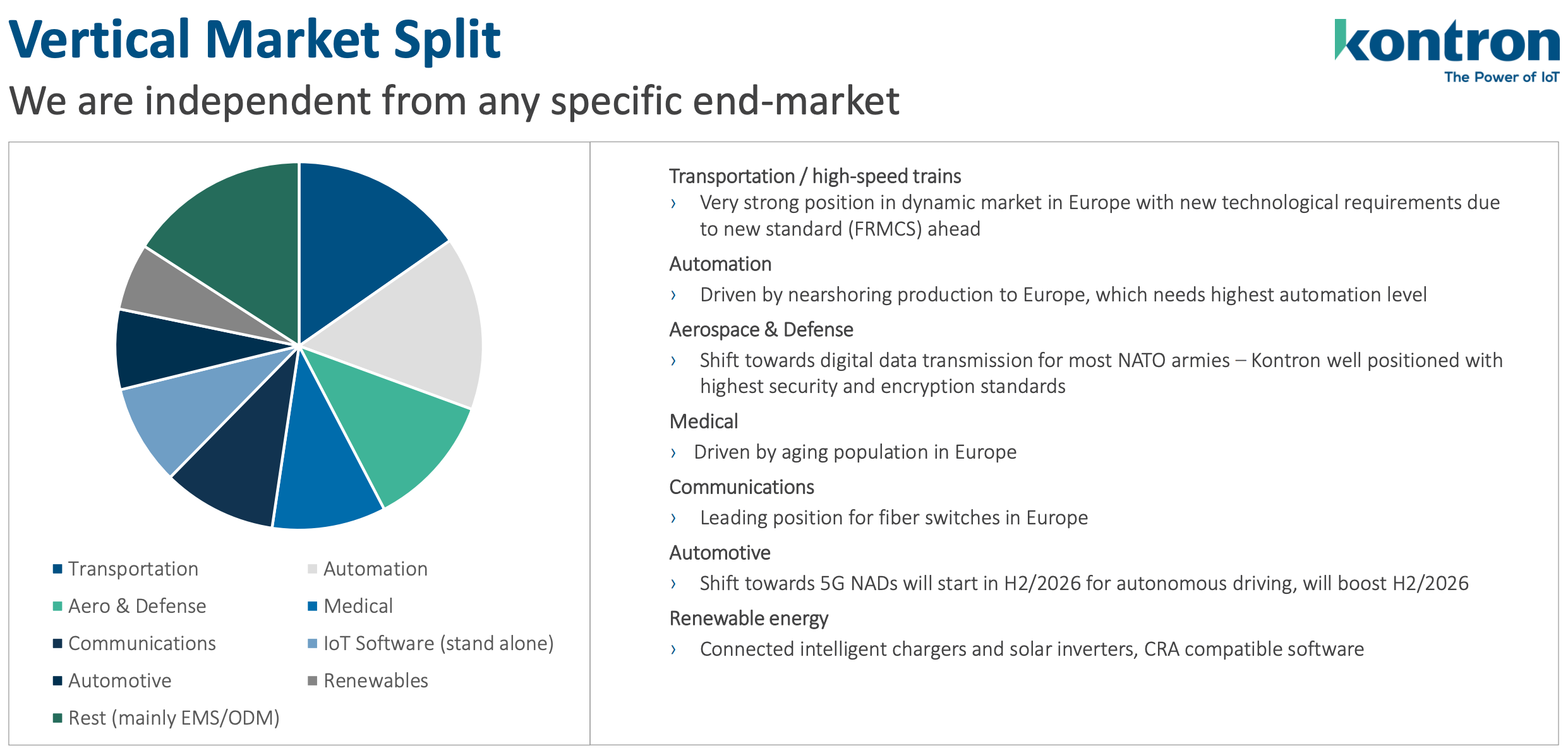

Cyclicality is there within many Kontron’s markets, but the sheer breadth of their offerings, reduce the Group’s cyclicality. Below, you can see breakdown by vertical.

The breadth of markets, check a box we like seeing for Niche Industrials — the ability to expand into more verticals. Where the technical niche give room for not competing on price, it’s the ability to expand into more verticals which gives room for the reinvestment of capital. If you have both, you got a recipe for compounding.

The success story of Ametek wouldn’t be what it is today if they didn’t expand beyond laundry machines and wastewater centrifuges with clever capital allocation.

Capital Allocation Strategy

Over the last decade, there’s two overarching Capital Allocation moves of Kontron. First, moving away from consumer products into networking critical applications, such as trains, aircraft, military equipment and robots. Secondly, the increased portion of sales towards software.

The best example of this is the recent sale of Kontron’s COM modules to their strongest competitor, Congatec, in 2024. This allowed Congatec significant synergies. What we found noteworthy, was that a part of the deal included a partnership between the two, where Kontron will equip future Congatec COM moduls with security software.

This move looks similar to what the semiconductor industry is well known for — specializing. With complexity increasing in Kontron’s industries, it seems they are confident moving up the value chain to the piece with higher margins — Software.

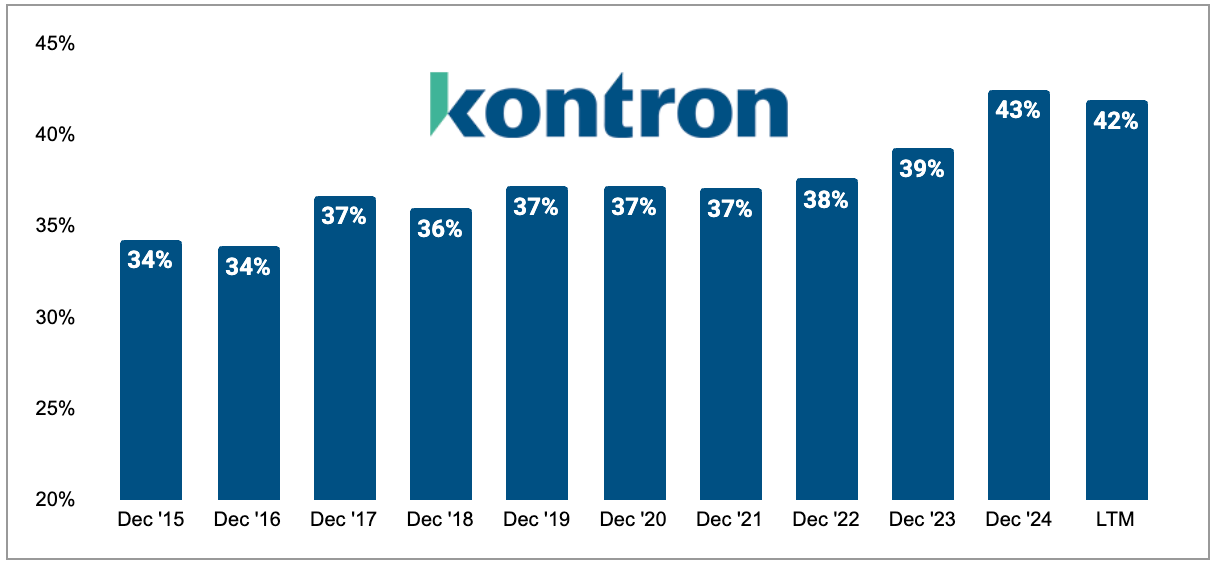

The increased focus on high-margin software and exiting lower margin businesses explains most of the significant gross margin expansion we’ve seen last decade.

A result of the Portfolio Streamlining is freed up resources within Kontron. Their focus is currently on 3 key areas:

Cyber Resilience Act in EU from 2025: New standards change the way the industry work, especially for high-stake fields like defence and infrastructure. Kontron OS is the first CRA compatible software for IOT solutions.

Companies are increasingly having to ask fundamental questions, like:

Are our devices updatable?

Do we meet CRA requirements?

How do we protect data flows in OT networks?

How do we modernize outdated but still used systems?

Kontron expects 100 million devices to be installed with this system until 2030, with a goal of installing more than 30 million by 2028.

Future Railway Mobile Communication Standard (FRMCS): By cooperation with Qualcomm, Kontron has become the only full solution provider for solutions that aim to deliver increased train safety and utilization of the rail network. FRMCS is expected to be mandatory from 2028, but most tenders specify this.

Network Access Devices (NAD): Also a result from cooperation with Qualcomm, is Kontron’s ability to take a leading position within the connectivity required for autonomous vehicles to detect digital traffic signs etc. Kontron already have orders above EUR 300 million, expected to start delivering this year (2026).

Our view is that Kontron’s strategy seem proactive.

Becoming the first non-Chinese supplier for certain automotive components or having majority market share within new standards for high-speed rail, does not seem like a coincidence. While others could follow, Kontron’s pace of innovation enables them the first-mover advantage, which strengthens their position as a trusted partner for many clients in adapting to new times / regulations / demands.

The Growth Opportunity

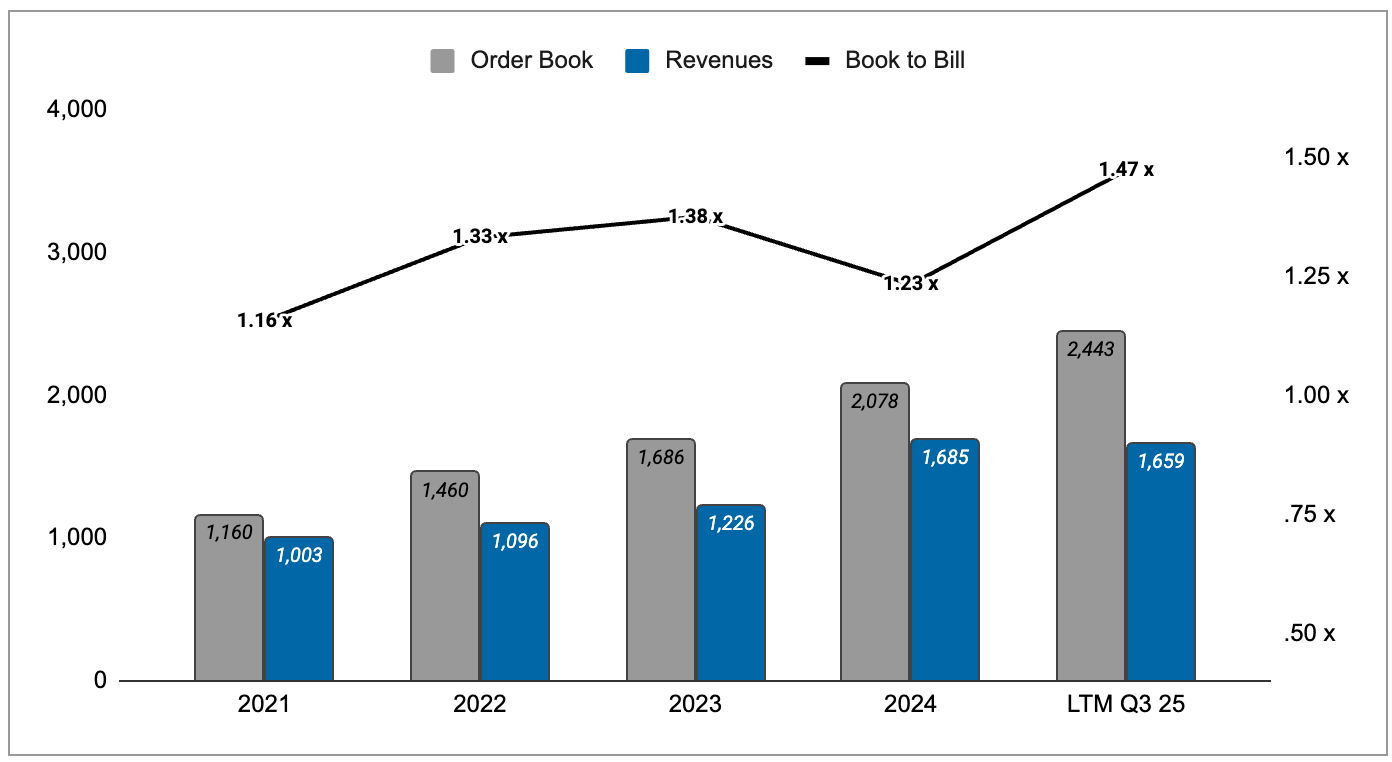

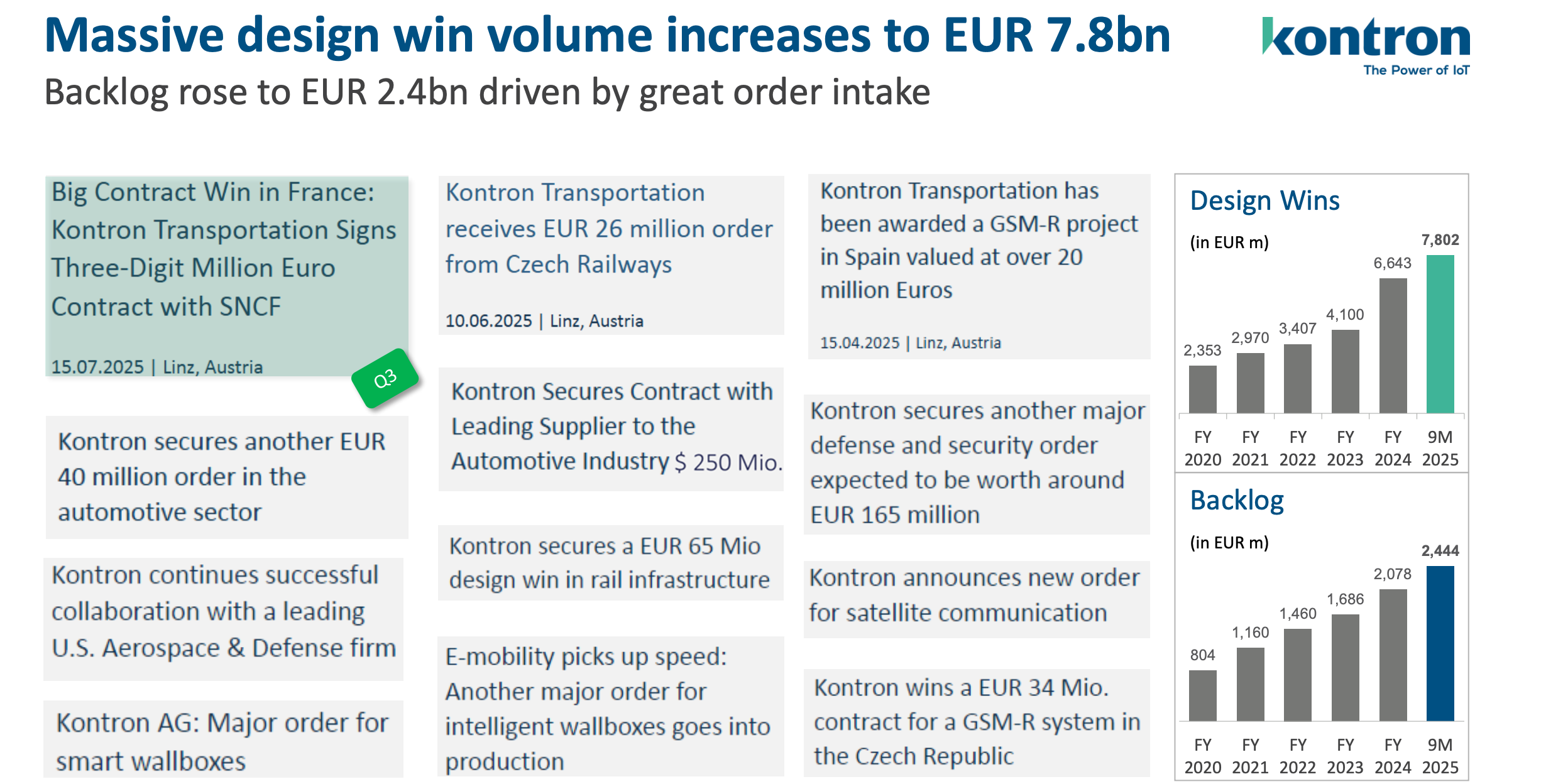

Kontron’s Order Backlog as of the Sep, 2025, was €2.44 billion, +18% since Dec, 24. That’s a Book-to-Bill ratio of 1,47x, signalling plenty of opportunity to generate growth.

This backlog comes from contract wins across many sectors, and some of the recent growth is also attributed to the Katek Acquisition in 2024. Kontron has also partnerred with notable much larger companies, namely Qualcomm.

Qualcomm’s General Manager, Nakul Daggal, said this:

“Kontron is one of the Industrial Leaders. It’s a company we really wanted to learn from and expand our portfolio along with them. In a really short time we established a lot of intersection points from connectivity to industrial processors. And because AI is part of all our products, we look forward to expand our partnership with Kontron”.

There is no doubt Kontron is on a winning streak when it comes to contracts.

With the market being especially intrigued with Defence exposure lately, it’s interesting to see the many defence related contracts. But where other IOT players like Curtiss Williams have seen massive multiple expansion, Kontron does not break out their Defence exposure in numbers.

As you can see below, Kontron stock has not benefited from a “Defence Label”.