Nordic Industrials - 2024

Top down view on a group of Industrials with a 7-year CAGR of 22%

This writeup aims to do a top-down view on Industrial Compounders from the Nordics. While this approach miss important details about each company, it is a good exercise to reduce bias towards your positions, and look at a bunch of similar companies from a new angle. Maybe, there is an investable idea in there as well.

As always, none of my writeups should be considered investment advice.

AMETEK - recipe of industrial success

Before diving into the niche Industrial companies from Scandinavia, let's begin with an intriguing case study. AMETEK, one of 8 companies studied by Mark Leonard in the creation of Constellation Software. This company, unfamiliar to most, have achieved remarkable growth, exemplified by a 100-fold increase in value over three decades—from $1.60 in 1991 to $160 today.

AMETEK´s strategy is quite brilliant. Operate within niche industries, requiring specific competence within one vertical, for then to reinvest the cashflows into other such verticals. Preferably, involving mission-critical products or components. Often, at a fraction of the total cost for the purchaser. Something like a small technical part of a fighter jet. This results in pricing power, enabling organic growth even if market share may be saturated. Anyways, due to the niche market, larger pockets will not be attracted to compete, enabling the potential to capture a first or second market position. This, being a premise to sustain high returns on capital.

As the ability to reinvest capital will be limited within one specific end-market, it makes sense to diversify the group by acquiring others. A beautiful recipe for compounding, if executed properly. Remember, buying a company with no growth at 5x profits, leads to 20% return on capital, if the asset can sustain it. If you can replicate this, you have something special. If capital is reinvested poorly, or at to high price, the end result may be closer to diworsification or even worse, destroy value by growth (ROIC < cost of capital). This has not been the case of Ametek, which have been a disciplined allocator of capital. Some intriguing facts of Ametek over the last 3 decades:

15% CAGR over 30 years = 12 800% total shareholder returns

EPS growth: $1 in 2009 → $5.8 today.

Return on Equity: 16% last 5 years

Operating Margins: 26%

Payout ratio: 18% = Ametek reinvests most of earnings

If you want to learn more of Ametek, I can recommend this episode, by Business Breakdown:

As we will dive into, the recipe behind Ametek should work just as well for Scandinavians. Perhaps even more intriguing, a place where less eyes are looking for them, despite plenty of them with favourable track-records.

INITIAL SCREEN

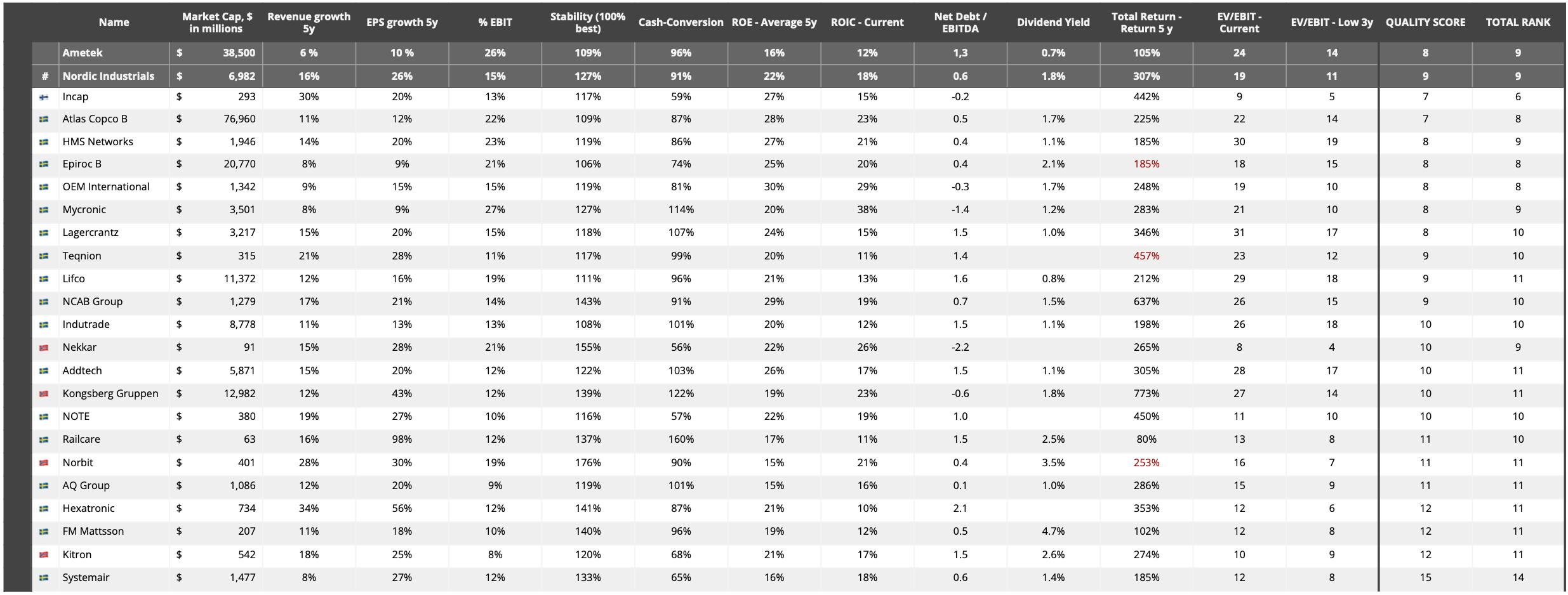

In an attempt to carve out a list of potential investable ideas, the below screen was made using Borsdata.se. Screening on 5-year results, with an average of >7% EPS growth, >14% ROE and lowest EBIT margins of >6%. A dozen companies where also excluded due to not selling physical/industrial products. Results are shown below, ranked in order based on how well they performed on the quantitate metrics used. Given the favourable screen criterions, it should come as no surprise all these companies performed very well over the last 5 years, averaging north of 30% returns per year. Although, the starting point for calculated returns were particularly favourable in this calculation, with most trading at multi-year lows mid 2019. For a 7-year period, returns were closer to 22% per year. Also, multiple expansion gave dual engines to the share-price over this period, with both EPS and valuation multiple increasing. Expecting this to continue forever, would be a fools errand. Anyways, let´s take look at the quantitatives behind these companies:

Scandinavian Industrial Compounders

Comparing AMETEK against the Nordic Industrials listed above, shows that the American giant is on average larger, more stabile and have higher margins. It also ranks in the upper half based on the ranking system I made. On the other hand, the Nordic companies grew much faster, with higher returns on equity, despite lower debt levels. In addition, they can be bought at lower multiples. The Nordics have also compounded faster, but if you take the weakening NOK and SEK into consideration - a Scandinavian owning Ametek would have done very well.

Atlas Copco seem to be the closest to AMETEK on all parametres - with the Swedish actually being twice the size. Epiroc, another high scoring company, spun off Atlas Copco some years ago, further solidifying the industrial company´s quality and track-record.

The difference in rank between the Nordic Industrials should be taken with a grain of salt. The higher interest rates are starting to show some industries struggling with demand, pricing pressure increasing & margins and revenue contracting. For example, the company ranking first, Incap - is struggling with destocking from their largest customer, resulting in a stark multiple contraction given the less favourable outlook this year. Further, Hexatronic is in a similar position, with reduced demand for their electrical components. Now, with 4 quarters in a row of declining revenues and EBIT margins (15% → mid single digits). An intelligent investor would research deeper, to find out if these are temporary declines, or if their fundamentals should improve again. By these historic measures, it sure looks like good companies at great prices.

Anyways, in a screen looking for the best companies, cyclicality or margin instability is not a favourable trait. Comparing Hexatronic to another company on this list, Lifco, underpins this. Another one not appearing in this list, Volati AB, is in a similar, but mixed situation. They have one division (Salix) struggling with cyclically low building demand & another (Etiketto Group) with stable earnings from selling recurring labels to manufacturers. Similarly between Etiketto Group and Lifco, these businesses deserves higher multiples compared to Sagax or Hexatronic, due to less cyclicality & recurring revenues.

With operating leverage being a dual-edged sword for companies with a lot of fixed costs, the EPS may fall much more than revenue in times of trouble. Consequently, the tempting valuation multiple may soon not look so cheap anymore, when revenue stops growing. Other companies in this screen also experiencing double digit declines in revenues, are Kitron and NCAB group. For NCAB in particular, the market assigns a pricey 26x EV/EBIT multiple. However, given their high quality score, track-record & CEO Peter Kruk hinting at better times, the market multiple may be more feasible.

We can see higher activity by many customers and the number of contracts won for new articles has increased. (NCAB CEO Q1 24)

Nevertheless, a prudent investor would conduct a much more comprehensive analysis of the individual companies than I have here, to determine their suitability for investment.

Valuation - Expensive can be cheap?

For the companies with low valuation multiples, one should ask: why this is the case? A company like Lifco, Atlas Copco or Ametek for that matter, may actually deserve a premium multiple. The reason I believe this, is that they all have a proven capital allocation strategy, with a decentralised structure and plenty of runway to grow (still only mid cap). Just look at the Dental division within Lifco, a recession proof, diversified and technology resilient business, making investors quite certain of it´s future outcome. Much more so, than most within this screen. These quality factors, sets these industrial giants up very well to continue reinvesting capital at high returns for a long time - the main driver behind compounding capital.

However, high valuation multiples come with inherent risks. If these multiples regress towards the 10-year average, overcoming this challenge would necessitate both ample time and sustained growth. Companies like Lifco, Addtech, and HMS Networks, trading at over 30 times EV/EBIT, may be particularly vulnerable in such scenarios. Moreover, if a company's growth rates or returns on capital decline, investors could face the daunting prospect of both diminishing earnings per share and contracting multiples. Even with a forward-looking horizon of 5 years, far surpassing the patience of the average investor, a doubling in EPS would yield no higher share-price if the valuation is halved. However, if a company can sustain high returns on capital >10% and prudently reinvest those earnings, valuation concerns may diminish over time. Nevertheless, historical trends indicate that investors might face substantial share-price declines of 20%, 30%, or even 50% during the journey - indicating that most of these, may become available at bargain prices from time to time.

All in all, the track-record, high returns on capital & reinvestment opportunities of the likes of Lifco, Atlas and Ametek, suggests the market believes these companies can continue compounding for many years to come - potentially justifying their premium multiples. It would be wise to study these in much greater detail, to find what price they could be attractive at. At least, it would be a fools errand, to expect the historic returns to continue as they have for all of these. Especially, given the unlikeliness of multiple expansion continue contributing positively to the share-price.

If you combine interest rates going up over the last year, with some industries experiencing cyclically low demand, you may actually find that some of the companies with highest multiples in this bracket will look “less expensive” in a year or two. On the other hand, buying companies facing short-term pain, such as Kitron, Hexatronic or Incap, at favourable multiples to historic earnings, may enable you to reap the rewards of dual growth engines for years to come (if things improve). However, there is no denying that buying industrial giants like Atlas Copco or Lifco, may be better “sleep-well” investments, and provide better risk/reward for many.

Dangers of Looking in the Rearview mirror

Relying on past returns to predict future performance is often a recipe for disappointment. It’s unlikely we’ll see 26% EPS growth over the next five years for the average industrial company on this list. Favorable conditions may have driven high returns on equity historically, and the companies not included might be heading for better times.

Anyways, the appeal of investing in quality companies lies in their ability to sustain high returns on capital over time, thereby avoiding mean reversion. When combined with ample reinvestment opportunities, as seen with Ametek, this creates a solid foundation for compounding growth for long times.

Ametek's low dividend yield signifies their capacity to reinvest cash flow instead of buying back shares. With a current return on invested capital around 12%, continuing to own Ametek could be rewarding, especially with some leverage boosting the return on equity.

Nordic industrial companies might offer similar opportunities, given their higher returns on equity, lower debt reliance, and strong growth rates. For instance, a company like Lifco creates value by continue to reinvest capital, given their consistent high returns on capital. Thereby, an owner may benefit the most if capital is reinvested. However, various factors might influence their choice to not do so with all cash. Such as the needs of majority owners, the opportunities available, shareholder preferences or a strategic approach to acquisitions.

Ultimately, future shareholder returns can be broken down into three factors:

Earnings growth = Return on capital * Reinvestment rate

+ Payout of earnings → Dividends or buybacks (leading to higher ownership)

+/- Valuation multiple changes

Observations - Scratching the surface

A big chunk of the companies in the screen, I must admit I´ve never heard about. But I´ve managed to scratch the surface of some. Let´s wrap up this one, with some interesting observations for the individual companies.

Bufab

Swedish Bufab, a company not appearing on the list due to its lower return on invested capital (10%), despite its strong return on equity (19%) driven by high leverage (3x Net Debt to EBITDA). Nonetheless, it deserves a mention for its impressive execution and substantial shareholder returns, boasting a 22% 10-year CAGR. Additionally, its value proposition is highly attractive to customers like IKEA.

Bufab exemplifies a common trait among many successful companies on this list: they handle complex, behind-the-scenes operations that are either technically challenging or highly specialised (niche), making them less attractive for others to compete against. Bufab also follow Ametek’s playbook by serving as an important but low-cost component of a physical product.

If large manufacturers like IKEA were to internalize their screw packaging, it would not only potentially decrease their operational focus but also increase working capital requirements and complexity, ultimately saving very little compared to the final product. Bufab’s ability to simplify and optimize these processes underscores its value proposition in the market.

Mycronic

Within the semiconductor industry, Mycronic sells machines within the photomask division, called Pattern Generators - with 65% EBIT margins last quarter. Probably helped by a mix of fixed costs and good deliveries in the quarter - leading to operating leverage. Still very impressive.

Mycronic´s business model, with hardware + aftermarket sales/service, have worked very well for the likes of european giants like ASML and Kone. Importantly, it helps even out the drastic fluctuations of hardware deliveries, and generate some recurring revenues. Notably, most of Mycronic´s markets are expected to grow high single to double digits until 2028.

Nekkar

Another company standing out in the screen was Nekkar, due to it´s valuation being of the lowest, despite good scores overall. Their main division, Syncrolift, have delivered 19 of the top 20 operational shiplifts globally. Although, some competitors, like Pearlson, may prove more fight for the upcoming project bids. Anyways, with ~25% EBITDA margins, 2 years worth of backlog and ~110million NOK in profit after tax, you can get all of Nekkar for 9x Syncrolift profits, with a strong net cash position. The other business lines does not contribute much to profits, but looks to develop quite decent.

Interestingly, the company initiated a buyback program in 2023, supporting that management find their own shares being an attractive investment.

OEM International

The returns on capital employed for OEM (40%) looking more akin to technology giants like Microsoft or Google, than the average industrial company. If you imagine Amazon.com for industrial components, you have something alike OEM. Every additional manufacturer/customer joining their platform, creates network effects - with the value proposition increasing with the number of participants within the network. This enables OEM´s solutions to become a natural tool in their customers daily work-life, and one quite hard to displace for competitors.

Atlas Copco

Nvidia have popularly been described as a shovel play in the AI race between the tech giants (referencing the shovel producers success in the gold rush). What is less known, is that the Swedish Industrial giant Atlas Copco is a shovel-provider to semiconductor producers in becoming more sustainable and efficient, by delivering products ranging from tightening tools to software. If you´d worry they lose out to other players in the semiconductor field, don´t worry to much - it’s only one of 12 large industries the Atlas Copco “conglomerate” serves.

Notably, while semiconductor production is mostly an automated process, the equipment working behind the scenes is not.

Atlas Copco is a strategic partner offering our customers a comprehensive pathway in their transformation to Industry 4.0 and fully connected Smart Factories.

Smart connected assembly tools for factories and field operations. Fully integrated assembly line solutions from design to production as well as a unique set of data driven services for more efficient, flexible, adaptable, and safe manufacturing processes. The result is reduced downtime, better use of materials and energy with a substantial waste reduction.

Introduction video to their semiconductor offering below:

Thanks for reading, I hope you enjoyed it. You can subscribe for free to receive my upcoming write-ups to your mail. Have a nice day :)