Shift4: Time for Weighing

Since Last Writeup, Shift4 Rejection of Takeover Bids Displeases Market. An opportunity to Reevaluate Fundamentals

If you are unfamiliar with Shift4, I’d recommend looking at my previous deep dive (#2), or read CEO Jared Isaacman’s shareholder letters. Jared (41), also known from Inspiration4 on Netflix, founded the company at the age of 16.

In essence, Shift4 makes tools for merchants to accept payments - a simple interface for guests, but a crucial tool for merchants. As Shift4 say themself:

One integration which can support every possible payment endpoint, and provide the most advanced business intelligence & analytics, giving customers the insight needed to run a succesful business. With redundant data centers & 24/7 support team, we ensure no unexpected outages. Shift4 is the last payment integration you need1.

To understand payment endpoints, envision a complex merchant like a hotel, where different providers handle payments in the lobby, restaurant, spa and for online booking. One tool for each unique task, creating barriers to seamless data flow and hindering the ability to learn from guest experiences. In addition to the hassle of dealing with multiple providers when service is needed. Consolidation of these endpoints presents an opportunity for an integrated payment processor, to offer the hotel a single provider/platform to meet all its needs.

Whether a merchant want to offer their guests ordering from the seat, QR-based payments, loyalty programs, online ordering or gain customer data from all payment endpoints - Shift4 unified payment platform has them covered. Whether the customer wants to pay with their debit, credit, apple pay or even crypto - doesn’t really matter, Shift4 can do it all.

Nonetheless, in the realm of payment processors, the extensive capabilities is only valuable when leveraged against a large volume of payments. As Shift4 has spent the past decade building this robust suite of capabilities, the strategic approach to acquisitions becomes clearer.

| Investors")

The Shift4 Strategy

We have a playbook and it isn’t complicated: We identify & acquire differentiated technology assets with an under-monetized payment opportunity. Either to grow existing verticals, or to reach new verticals/geographies. Not only has our strategy afforded us the ability to offer merchants a value proposition previously unavailable in the market, it has also resulted in our growth consistently exceeding industry averages (CEO)

This value proposition, unlike the network owners (Visa/Mastercard) charging network fees for connecting banks, is targeted to assist merchants delivering a seamless guest experience. As a large chunk of the payment revenue goes to network fees, Shift4 is left with sub 30% gross margins - demanding operating cost discipline. Also, cross-selling makes sense, since the customer acquisition cost & operating expenses serving one merchant, don´t scale proportionally to a potential revenue uplift. To illustrate this point, consider the following (favourable) hypothetical scenario:

Imagine Company A, offering loyalty shop applications to stadiums across the US, for a subscribtion fee. Although they generate revenue, profitability is minimal. This represents an under-monetized payments opportunity.

Shift4, with their integrated payment capabilities, acquires company A for, let’s say 10x cashflow, and gives away modern point-of-sales machines for free - to remove friction and enable recurring payments revenue. Also, Shift4 stops charging $ for the loyalty application company A once charged for. In addition, Shift4 offer a substitution for other software programs the merchant paid for at a low total cost/or for free (websuite builder, staff management, analytics etc).

Short-term, this reduces the potential revenue pool for Shift4, but, don’t mistake this as a fooled strategy. Giving away scale benefits to customers, such as Amazon and Costco have done for decades, creates a value proposition incredibly hard to replace - leading to customer loyalty & switching costs.

Now, you can find Shift4 powering everything from the loyalty shop, concession stands to building webpages. Integrating all these applications to one provider, Shift4, enables the merchant to seamlessly capture and analyse guest data, further strengthening the value proposition. The following year, Shift4 also “win” the ability to process ticketing volume for some of these stadiums, a potential >10x uplift in volume. Shift4 can now power a merchants many needs, with less employees per $ of revenue captured → operating leverage.

Within 2-3 years → succesful acquisition x cross-sells = strong ROI

Cross-selling → Operating Leverage

In the hypothetical scenario outlined above, the revenue uplift post-acquisition should coincide with relatively flat operating costs, resulting in operating leverage. Moreover, by utilising one integrated payment processor, merchants can more easily capture value from guest data, illustrating the thesis presented in my initial deep dive: Shift4's transition from a point-of-sale distributor to an operating system.

As traditional point-of-sale machines only address a fraction of a complex merchant's needs, there is ample opportunity for Shift4 to cross-sell a variety of services at low marginal cost. These services may include subscription-based offerings such as inventory and staff management, advanced reporting, business intelligence, online ordering, and website hosting. To exemplify Shift4's wider impact than only payment terminals, consider the testimony from this year's Super Bowl host, Allegiant Stadium:

“We were looking for a partner not only to create a first class venue, but also take us to the future… The NFL fan survey voted Allegiant as the best stadium in the world.”

Allegiant Stadium's choice of Shift4 wasn't merely for receiving point-of-sale machines for free; rather, they selected Shift4 as their preferred partner in enhancing the guest experience. Furthermore, the substantial increase (2x in 2 years) in subscription revenues, represented by the dark blue columns below, further underscores Shift4's evolution toward becoming an operating system for merchants. Importantly, subscription revenue has higher margins.

However, amidst this growth via acquisitions lies the less glamorous aspect: debt, currently standing at 3.5 times EBITDA. Yet, management has benefited from low interest rates (fixed ~1%), resulting in net interest payments in 2023 amounting to a mere 0.5% of revenues. While some may attribute this to luck, my observation suggests that management has displayed exceptional capital allocation skills. This trait is undeniably attractive, particularly for a business generating substantial cash flows. With a track-record of consistent growth for two decades prior to going public, without the need for outside financing - they took advantage of low rates to reaccelerate their growth trajectory.

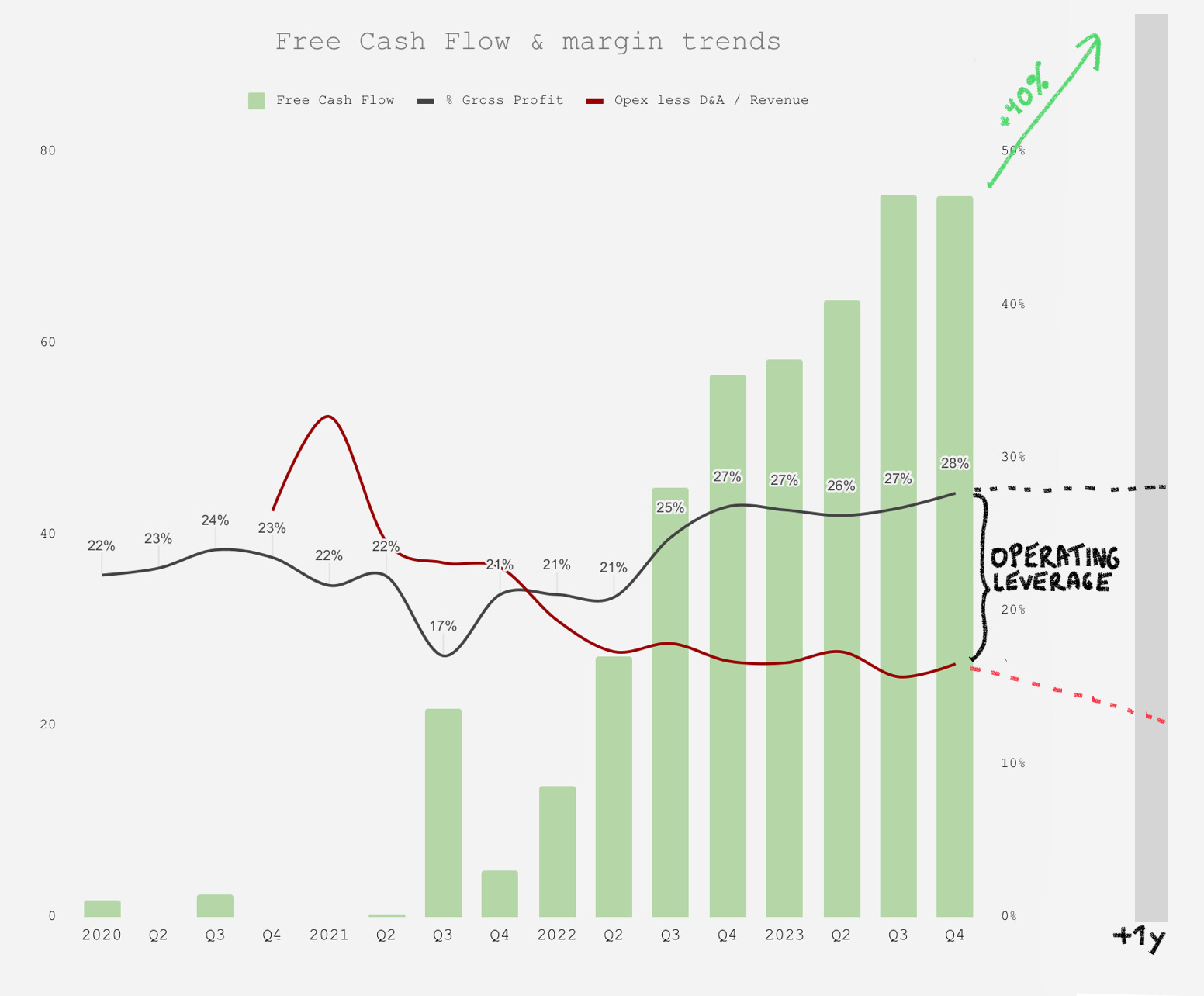

Cashflows trumps Profits

As Shift4 accelerates growth, the income statement look poor. Here's why: Their strategic approach, which involves acquiring technology assets, often at premiums well above their book value—results in substantial amortisation expenses in the subsequent years. Moreover, the decision to distribute point-of-sale hardware for free necessitates depreciation expenses. While these costs have been significant in recent years, they are accounted for as consistent annual expenses, despite being one-time cash outflows. Management have previously stated they earn back the investment in 2 years.

After deducting depreciation & amortisation expenses, you get a large discrepancy between the income and cashflow statement. Especially, when you grow 40% a year, like Shift4 does. To illustrate, Shift4 recorded $400M in free cashflow2 over the last 2 years, but only $210M in net income. Noteworthy, the 2024 guide includes $350-400M in free cashflow, (~50M less when subtracting stock-based compensation). This means Shift4 may do free cashflow this year, close to the last 2 years put together. What should a company growing cashflows like this be priced at?

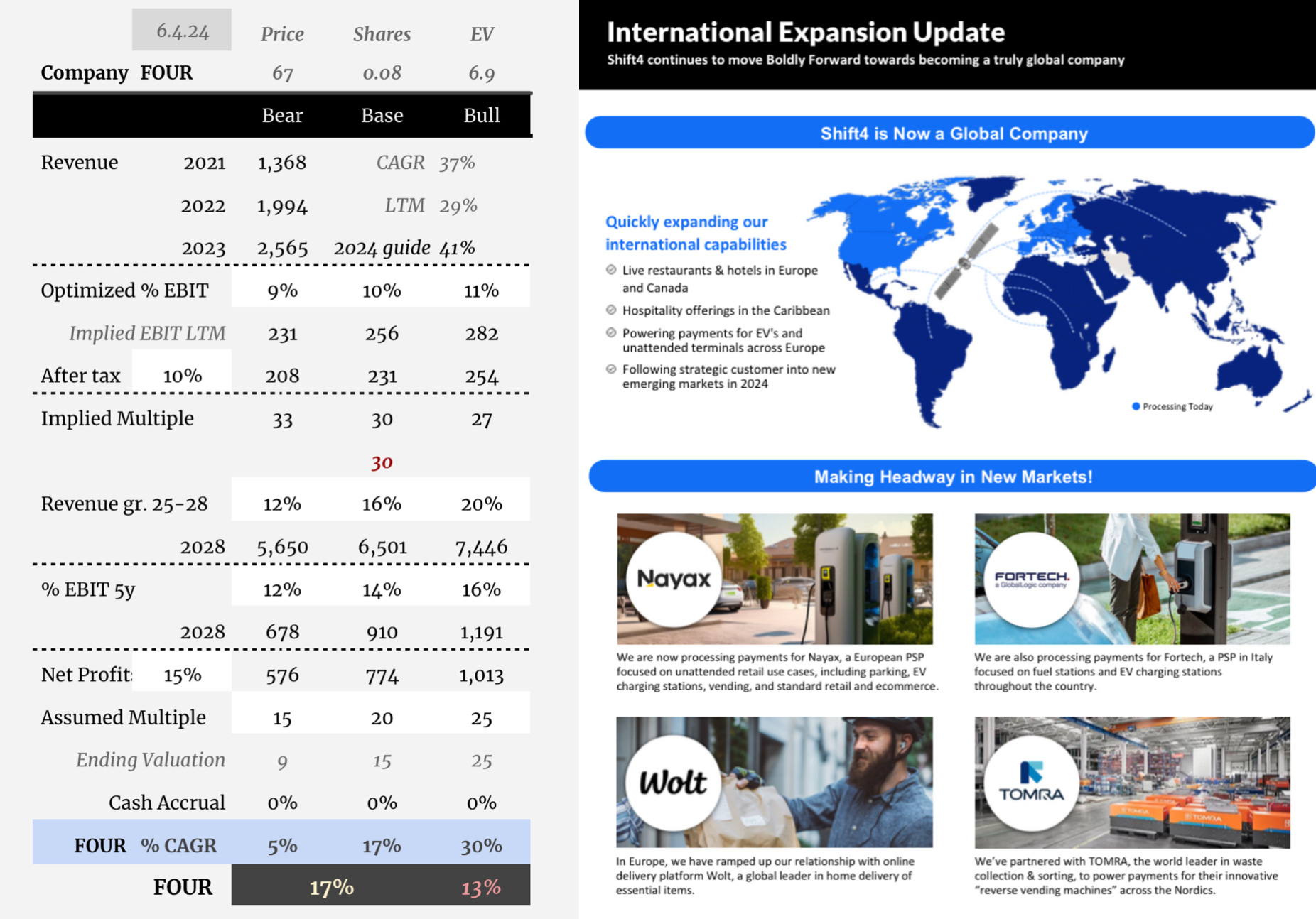

2nd floor valuation for skyscraper growth

In the long run, the market is a weighing machine (B. Graham)

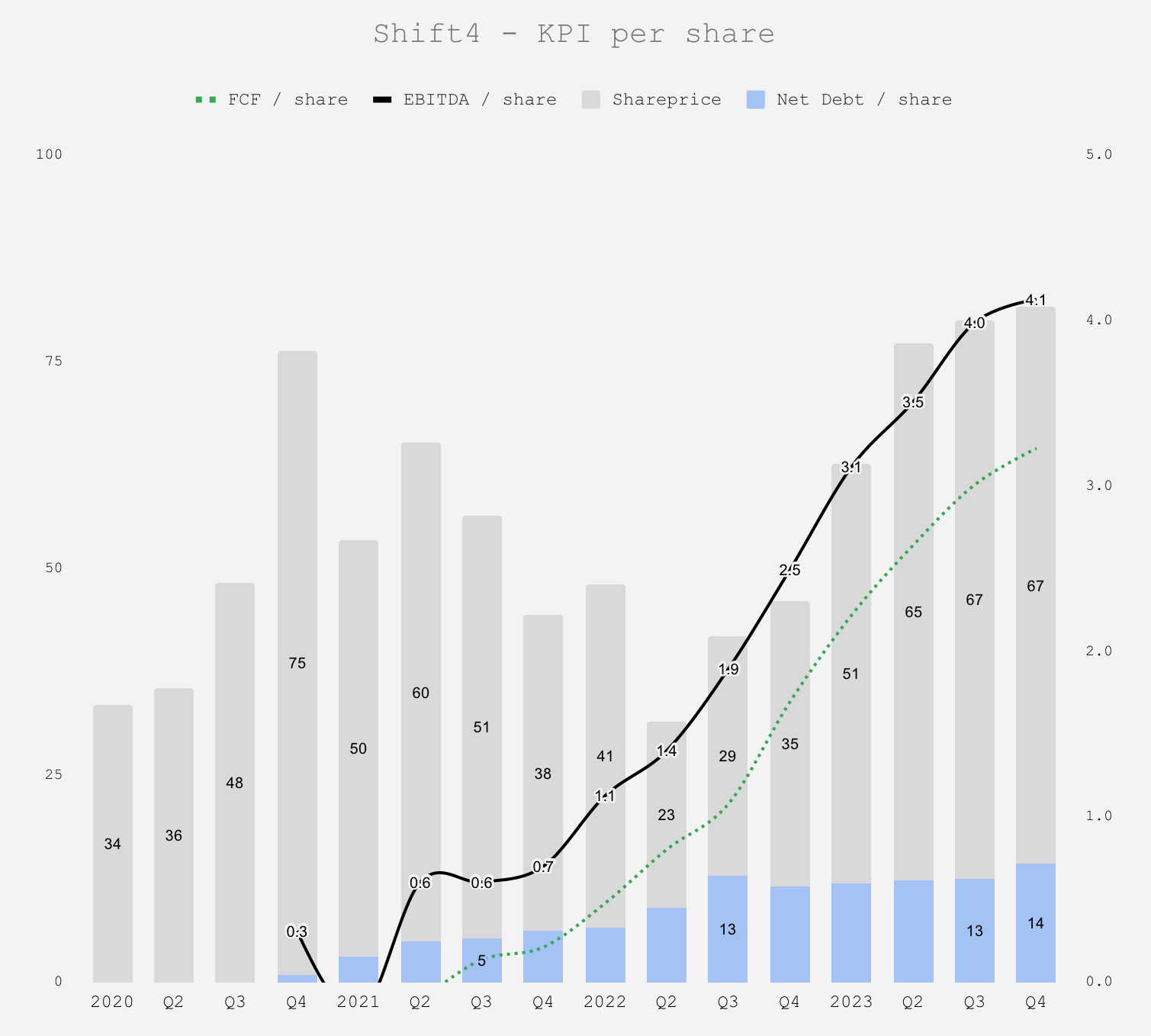

FOUR is priced at $67 per share / $5.8B market cap / $6.9B enterprise value. While the share price has surged 40% since last update, the stock still look relatively cheap, if they can execute on their 2024 guidance, of:

Revenue less network fees: +38→44% (+35% in 2023)

Adj.EBITDA: $635 → $675M ($460M)

Margin: 49-51% (49% in 2023)

Free cashflow-conversion: >58% (42% in 2023)

In total: ~40% revenue growth & FCF margin expansion → >40% FCF growth. In line with the 5-year valuation model below, 15-20x this years cashflow sounds attractive, especially given the recurring nature of payment revenue.

https://www.shift4.com/partners

Free cashflow = operating cashflow - Capex - stock based compensation

Thank you for your interesting contributions.

Whats about competition?

On the first look I would say, I see in europe not stock listed payment processors with similar enhanced features (analytic tools etc.) ( e.g. https://www.sumup.com or https://www.orderbird.com or https://www.clover.com/ --> part of fiserv)

I some stores you can already buy your SumUp mini terminal while buying your weekly groceries.

The only difference I can see for now is that shift4 don't charge any cost in upfront for the hardware. But that could be easy copied by the competitors.

I find it difficult to recognize the lasting competitive advantage.

Perhaps you can shed more light on the competitive landscape in an update.

I have also read that fiserv would like to take over 4shift.

Phenomenal business run by an intelligent fanatic. The recent Nuvei transaction gives legs to the overall private market valuation and drives my confidence in buying more into $FOUR at the $63 levels. Thanks.