Inside the Corner - May 2025

Lessons from Recent Writeups — and a Look Under the Hood of Our Investment Journey

Since the March update, three new writeups have gone out—and the response has far exceeded expectations. It’s incredibly rewarding to see the work resonate, even though I also appreciated the quiet early days when no one was reading. The mission remains the same: to keep improving.

Thank you for the support—every like, message, and comment truly matters. And a special thanks to the new paid subscribers since last time. There’s a dedicated section at the end just for you.

Below are links to the 3 latest writeups.

Main Lessions since last time

The two writeups on MBB and Topicus highlighted two key lessons:

1. Look under the hood of holding companies.

To properly evaluate them, we must first understand their structure—especially ownership stakes in subsidiaries and other minority owners. After this, we can assess the quality of the underlying assets, the reinvestment engine, the returns on incrementally invested capital, and the competence of management. If any of these factors can’t be understood clearly (directionally right at a minimum), the company belongs in the “too hard” pile - where we placed Exor (for now).

2. Working capital dynamics matter more than you think.

In the case of Topicus, we saw the advantage of structural negative working capital—unlike most industrial acquirers, which often need to tie up cash in inventory and receivables to grow organically. While many businesses with positive working capital can be excellent compounders, those that scale efficiently without it often generate stronger cash conversion. We view the EBITA/Working Capital metric used by companies like Lagercrantz and Momentum Group as a gold standard—one metric (or similar) more industrial companies should adopt. Serial acquirers often shine here, as their focus on inorganic growth makes free cash flow a top priority.

If we find a capital intensive business where they do not report or at least discuss the returns surrounding their capital allocation decisions, we are out.

Measuring profits before growth investments—such as working capital outflow, capex, and M&A—sharpens our understanding of the capital allocation decisions behind growth investments—or the absence of them.

Lastly, the recent analysis of Owner Operators underscored key-man risk, exemplified by the founder's departure from Shift4 and more recently, Warren Buffett's planned departure from Berkshire Hathaway. The Wallenberg family within Investor AB have continoussly stressed the importance of careful board selection and active participation. For investors in owner-operated or founder-led companies, this may be something to watch more closely, as this may suddenly become reality.

Portfolio Performance

Year to Date the portfolio is up 4%, with 3 companies pulling the portfolio - MBB (+62%), Norbit (+53%) & Topicus (+35%). While we’ve had many losers as well, most recently our smaller stakes in Evolution and Nilörn (so far), the winners have more than made up for these mistakes.

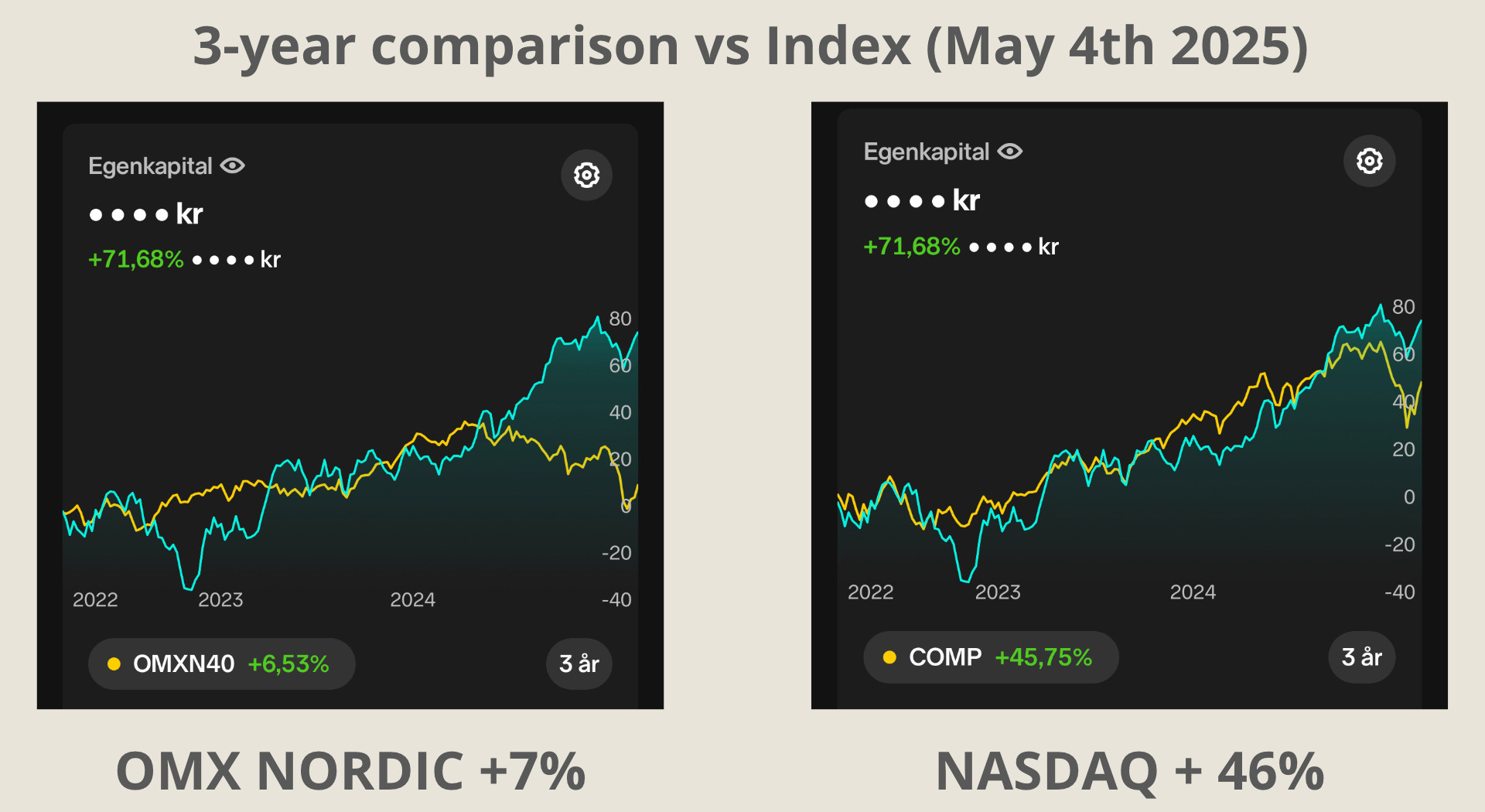

Over a longer time span (72% in 3 years), we have probably had our fair share of luck against the indexes. Returns have also been helped somewhat by weakening NOK.

Meanwhile, key OMX Nordic index constituents such as Novo Nordisk, Atlas Copco, and most of the Norwegian energy sector—typically more reliable performers—have been out of favor. That’s unlikely to last forever.

Still, we’re not focused on not owning the Nordic heavyweights or the Magnificent 7 in the US. What matters most is peace of mind: holding companies we understand deeply and can comfortably own through cycles. That often means steering clear of headline-driven stocks—and those are exactly the kinds of ideas we aim to share here.

If you have suggestions for topics you'd like me to cover in future writeups, feel free to reach out—I'd love to hear your thoughts.

The remainder of this writeup is reserved for paid members and includes a deeper dive into the portfolio, individual positions, and the actions I’m taking. Most company and sector overviews will continue to be available for free.

If you're considering subscribing—whether to support my work or to access the full monthly updates and additional content—you're very welcome to do so below.