Portfolio Update

Introduction

This retrospective is primarily for my future self, to capture the mindset and strategies that shaped my decisions. If one other finds value in it, that's a bonus.

My goal in investing is not to achieve perfection but to pursue continuous improvement—a mindset I also strived for during the 8 years I lived as an endurance athlete. It´s easy to sit here with the benefit of hindsight, and call out what should have been done differently. Rather, want to learn from past mistankes, and try to focus on the future. Hence, why I've chosen "The World in 2050: How to Think About the Future" as the first book on my reading list this summer.

Looking Back: Portfolio Performance

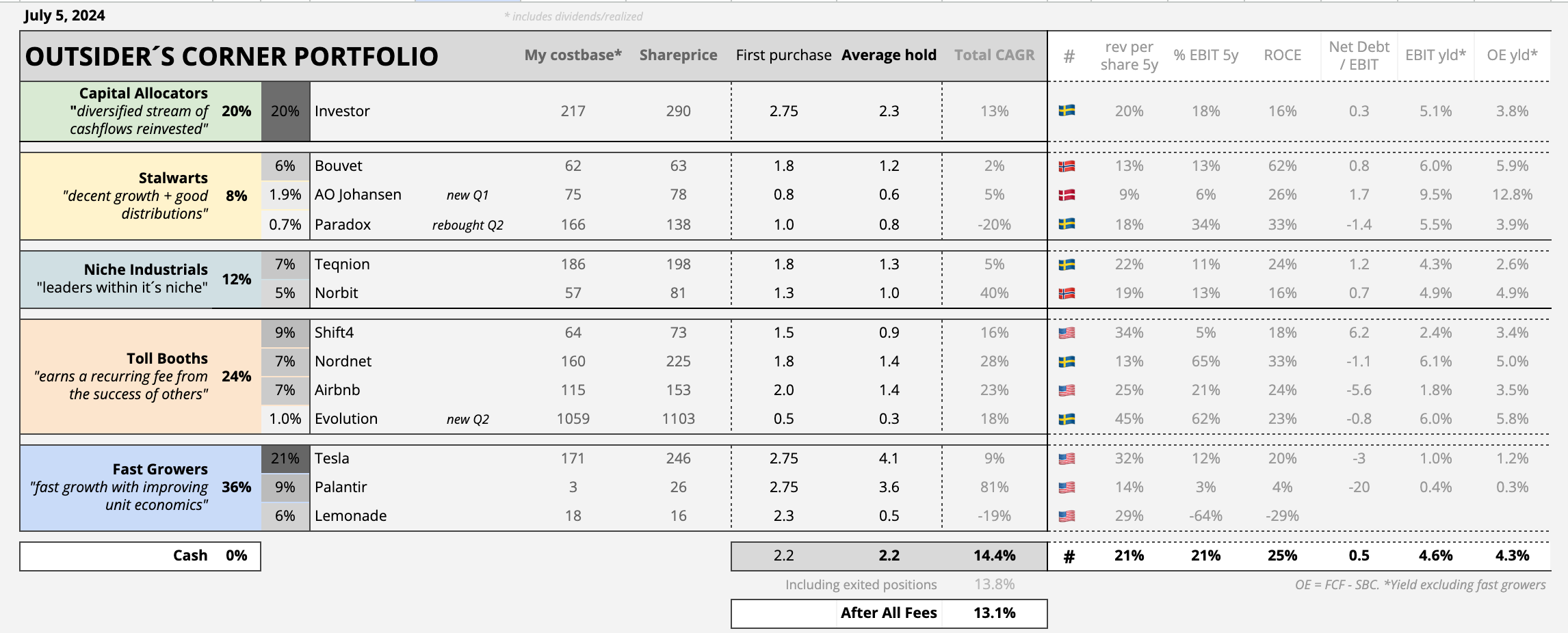

Since the start of my portfolio, it has delivereded a total return of 13,1% per year, or +30% in total over the 2,5 years I have been investing. Excluding the bad stuff, realized gains/losses in exited positions (-0,6%) and brokerage fees (-0,7%), returns would be 14,4%. Going forward, I should try to reduce brokerage fees, by purchasing stocks as I do with toilet paper: Big bulks and on discount, and of course, not reuse them (trade).

I will not go deep into the weakening currency improving these returns, and the recent spike in some shareprices, as I try to focus on the business fundamentals. However, my returns are not much to applaud. Most of the time underperforming the market and with more volatility. When it comes to business fundamentals, I measure growth (21%), margins (21%), capital returns (25% ROCE), leverage (0.5 Net Debt/EBIT) and valuation (4,6% / 4,3% EBIT and Owners Earnings yield) as KPI for the portfolio. While I excluded the Fast Growers from these calculations, the numbers should reflect my focus on quality and longevity.

Classification of Companies

After the early mistake of investing too much capital in speculative, unprofitable companies, I realized that holding many such stocks together does not provide effective diversification. ARK Invest is a prime example of this, with a portfolio of companies that often move in tandem. Subsequently, they may face structural disadvantages compared to individual investors. This is because they receive more inflows when people are eager to invest in speculative assets (when prices are higher) and fewer inflows when their holdings become cheaper. Literally, buying high and selling low. Moreover, since most of their compensation is tied to accumulating assets, they are incentivized to focus on size rather than performance, like most fund managers.

It also wouldn’t help to provide investors with look-through earnings per fund unit, as there are few profits to show. While I appreciate ARK's transparency and sharing of research, I'm glad I eventually sold my position—it was one of my earliest investments and, unfortunately, the one I lost the most capital on.

Reflecting on this, I see the importance of owning companies with different business models and varying strengths and weaknesses to achieve true diversification. Consequently, I have divided my portfolio into some categorizes.

Capital Allocators

diversified stream of cashflows reinvested

Growth: 20% // EBIT margin: 18% // ROCE: 16% // Net Debt to EBIT: 0,3 // EBIT yield: 5,1% // OE yield: 3,8%

In investing, it often pays being a passenger on someone elses brilliance. Investor AB being a prime example of this. Their portfolio holds strong market positions in industries with durable tailwinds, such as industry, healthcare and technology.

Owning a stake in Investor allows you to benefit from the growth in the earning power of its underlying companies, the reinvestment of Investor’s cash flows at good returns, and the dividends received from Investor—in that order. Additionally, there's the conglomerate discount to net asset value, which fluctuates with the stock market.

In the short run, the stock market is a voting machine. In the long run, it´s a weighing machine (Ben Graham)

Stalwarts

decent growth + good distributions

Growth: 13% // EBIT margin: 17% // ROCE: 40% // Net Debt to EBIT: 0,4 // EBIT yield: 6,7% // OE yield: 7,3%

Stalwarts provide the portfolio with steady cash flows. These are quality companies with longevity. Generally, if a company can reinvest cash flows at high returns on capital, investors benefit. However, Stalwart companies often hold leading market positions, limiting their reinvestment opportunities or the speed at which they can deploy capital. This makes dividends to shareholders a sensible approach. Divesting outside their core or making poor acquisitions could dilute the quality. Nevertheless, I like seeing them reinvest either organically or through acquisitions which meet their hurdle rate, as they have a good track-record of doing so. Recent examples include acquisitions by AO Johansen (VVSkupp) and Bouvet (Headit).

Paradox is the recent addition to this category, a company I owned previously. You will soon find a detailed writeup on them by

and me.

Niche Industrials

leaders within it´s niche

Growth: 21% // EBIT margin: 12% // ROCE: 20% // Net Debt to EBIT: 1,0 // EBIT yield: 4,5% // OE yield: 3,5%

After my recent analysis of Scandinavian Industrial Compounders, I had to create a category for these types of businesses. Niche industrial companies thrive in monopoly or duopoly markets due to their limited size. Larger companies typically avoid these small markets, allowing smaller teams to develop valuable know-how and protect their margins from competitors.

A common challenge for niche industrials is finding reinvestment opportunities. However, companies like Ametek in the US have shown how to do so effectively. I prefer niche industrials with strong strategies for redeploying capital. Developing new niches is difficult, but acquiring other small niche players may be a more replicable and durable strategy. Teqnion is a key example being a serial acquirer, and Norbit's recent acquisition of Innomar illustrates this approach as well.

I have started purchasing another niche industrial company, but more on that later (hint: it's mentioned in the sector writeup below).

Toll Booths

earns a fee from the success of others

Growth: 29% // EBIT margin: 38% // ROCE: 24% // Net Cash // EBIT yield: 3,5% // OE yield: 4,0%

Toll booths—those you pass every time you drive—are a perfect analogy for these businesses. Consider the payment fees charged every time you use your credit card, the small cut taken by the developer of your favorite casino game, the commission earned by the facilitator who finds you a beautiful coastal rental for your holiday, or the brokerage fees incurred with each stock trade. These businesses thrive on recurring, incremental fees, making them akin to modern-day toll booths on the path to profitability. With high fixed costs, network effects, a powerful brand, switching costs or scale economics, they are often extremely difficult to disrupt. Sometimes, regulation may come in - if they are creating more trouble than good.

Shift4, Airbnb, Nordnet, and Evolution Gaming are my current picks. The key to assessing such companies is to consider whether they thrive on win-win relationships. Does the merchant gain a clear advantage by using Shift4 over other providers? Is Airbnb providing genuine value to property owners, or are they taking an excessive portion of their revenue? Could an online casino feasibly develop its own live casino games instead of relying on Evolution Gaming, or would they lose customers in doing so? These questions are crucial in identifying businesses that benefit from mutually beneficial relationships. While some companies rely on high switching costs to retain clients despite dissatisfaction, I prefer win-win situations where your customer is your partner. If your customers grow, you grow. Win-win.

One of the best businesses to own is one that earns a fee off of other people's money (Warren Buffet)

Fast Growers

fast growth with improving unit economics

Growth: 25% // EBIT margin: 7% // ROCE: 12% // Net Cash // EBIT yield: 0,8% // OE yield: 0,9%

And now, onto the more controversial picks. These companies are frequently discussed on X, drawing in a diverse mix of fans, short-sellers, all-in investors, and attention-seeking fund managers. Getting a balanced take on these can be rare, as reality may be somewhere between all these opinions. Understanding them can be daunting, reflected in their volatile share prices. While it may be prudent to steer clear, I believe in following Peter Lynch's advice: know what you own and why you own it.

Despite the noise, companies like Tesla, Palantir, and Lemonade remain steadfast in their long-term strategies to enhance their competitive edge and capture market share in massive industries. However, their potential outcomes could vary significantly. For me, confidence in management, proof of an exceptional product, and me entering at a favorable buying price are crucial considerations.

Take Tesla, for example. Despite its current financials reflecting an overvalued cyclical auto business, my average purchase price of $170 factored in future growth potential in automotive and energy, and not in other areas. By not accounting for optionalities like autonomous driving or robotics, these options become essentially free. However, there is massive downside if I am not able to accurately price Auto + Energy, given the demanding valuation. Since these assumptions will be wrong, I´d rather be roughly right than directionally wrong. Tesla's recent spike in operating expenses, driven by significant investments in Nvidia GPUs, also signals its doubling down on autonomy.

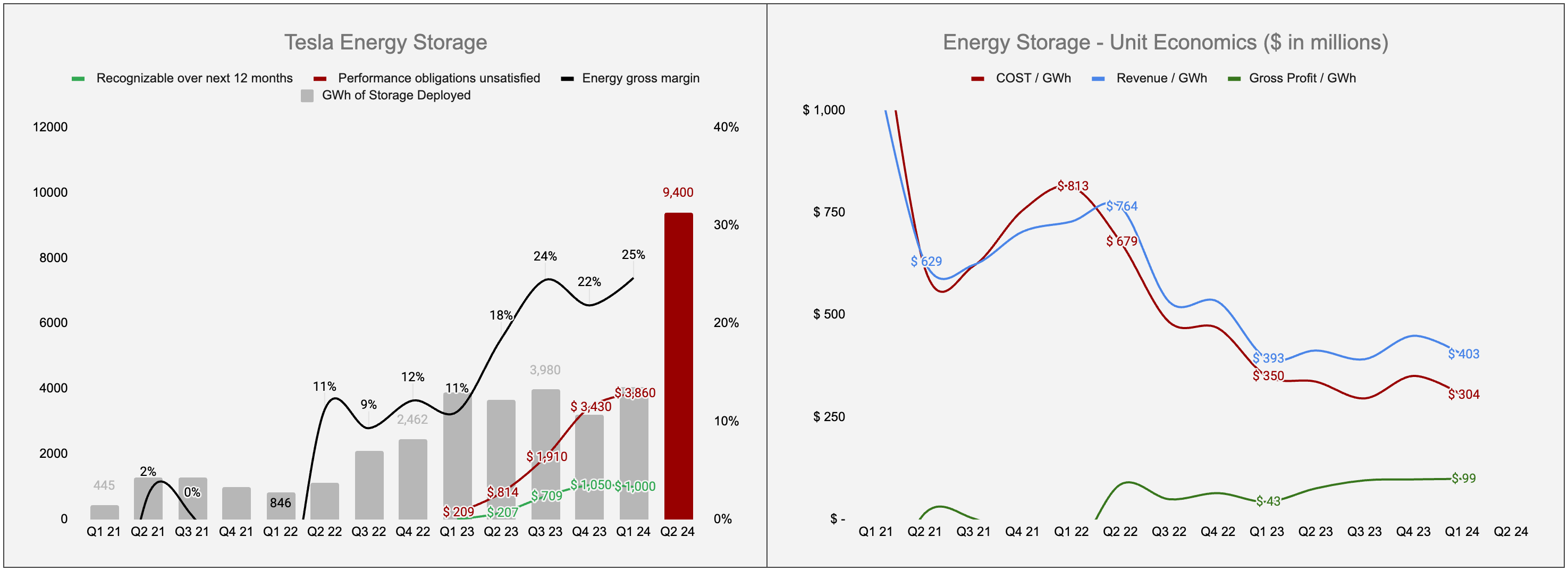

My contrarian stance on Tesla includes two key points: First, widespread autonomy adoption may take time, but if Tesla's vision and neural net strategy are correct, it may already have secured a substantial competitive advantage. Second, Tesla Energy could surpass automotive gross profit within 2-3 years. With the opening of another Megafactory in China, capacity may reach 80 GWh in a couple years. Recent upticks in energy deployments and importantly, performance obligations starting to cash in. As Tesla continues to lower costs per GWh, traditional gas peaker plants should take notice. Analysts have yet to fully recognize this potential, making Tesla Energy a hidden gem (less so after Q2 numbers) within the company's portfolio.

KPIs for Energy Storage: Notice the recent uptick in deployments in Q2 2024 (red bar). While some of this may be due to timing, an annualized run rate of two factories could double this runrate and potentially generate over $10B in gross profit in a couple years, with remaining performance obligations contributing somewhat delayed to the profits. Remember, depending on how well Tesla´s storage systems perform, the buyer pays performance obligations. If these does not work as expected, Tesla have to pay. With the recent uptick in recognizable amounts this year and gross margins increasing, I believe there are signs Megapacks are working more than good. In simple terms, this means revenue flowing straight down to the bottom line.

I'll delve into Palantir in a separate write-ups - which will cover their story from Battlefield to Business. I may have to consider not trimming my winners that much going forward, but 20-30% in PLTR 0.00%↑ felt to much. I´d rather have good sleep.

Lemonade

Lemonade, once a meme stock, has since fallen 90% despite improving fundamentals. EV / Sales multiples have ben cut tenfold, and you can now basically acquire 1 insurance customer for ~30 shares of $16 shares of LMND 0.00%↑. Some of my thesis can be summarized below:

>3x Lifetime Value (LTV) / Customer Acquisition Cost (CAC) ratios. This is achieved by targeting low-hanging fruit customers (young, renters, pet owners). Remember, LTV is already discounted back to present value of cashflows, meaning any value above 1 should create value.

Increased their ability to offer more insurance policies, allowing cross-selling as customers age (improving premium per customer and retention rates). Lemonade´s customers spend >10x less than those others = grow w/ customers.

Improving loss ratios, if this is due to the effectiveness of their AI pricing model or just rate changes (finally) coming online, remains to be fully seen.

Flat operating expenses while In-Force Premiums has multiplied, indicating they only need more scale to become profitable.

Lemonade has addressed their cash burn rate through the use of what they call synthetic agents. These (General Catalyst) help fund the Customer Acquisition Cost (CAC) and in return receive a decent IRR over two years. This strategy makes Lemonade own all the customer´s profits after year 2, unlike most insurance companies that must share revenue with insurance agents indefinitely.

Priced slightly above their net cash position, Lemonade presents a highly asymmetric bet, especially as they guide for cashflow breakeven next year. While they previously were priced to disrupt the insurance industry, I´d argue the price today reflects more a company about to go bankrupt. There is still risks to be aware of, but it has improved. Looks like management believes the same, as they have been buying Lemonade shares over the last weeks. I will leave it with this quote from Jeff Bezos.

People always excused us for selling a dollar for 90 cents. But that was not what we were doing. We always had positive gross margins. It’s a fixed cost business, so what I could see from the internal metrics is that at a certain volume level we would cover our fixed costs and become profitable (J.Bezos, 2006)

Path Forward

One of my key realizations is that survival is more important than finishing first. At 26 years old, I don’t need to achieve 20%+ returns to be successful. Most of my capital will be deployed in the next decade, with a significant portion coming this autumn after a real estate sale. This makes it an especially good time to establish a solid foundation.

Regarding hurdle rates, I aim for 15% rate of return. If I were seeking 10% returns, I might as well just invest in a global index. I try to keep relatively straightforward calculations, such as those for Bouvet, where I estimate approximately 10% profit growth plus a 4% dividend yield, with a similar terminal multiple. On the other hand, targeting above 20% returns could lead to missing great opportunities in wonderful businesses that rarely become that cheap. Additionally, I don't believe I have the ability to achieve those high returns consistently, and they would probably lead me to more speculative bets.

So, how can the portfolio achieve more downside protection? The first step is likely to reduce the allocation to the fast grower category (currently at 36%). I´ve also learned a lot diving into AO Johansen, which has a much lower valuation multiple than most of the portfolio companies, meaning the markets have already priced in that it doesn´t go that well. With history having shown repeatedly that many of yesterday’s winners continue yielding good results, there's no need to constantly find new winners. Additionally, I think I could add a couple more holdings (15-20), allowing my portfolio to naturally concentrate over time. Here’s a potential allocation strategy:

Capital Allocators: Currently: Investor AB // 20% → 25%

Stalwarts: Bouvet, AO Johansen, Paradox // 8% → 12%

Niche Industrials: Teqnion, Norbit // 12% → 12% (recently added one more)

Toll Booths: Shift4, Nordnet, Airbnb, Evolution // 25% → 25%

Fast Growers: Tesla, Palantir, Lemonade // 36% → 25%

Let’s wrap this up. Thanks for reading, if you came this far. Going forward, I am working on some larger writeups. I would also welcome feedback if you find a portfolio update interesting. It will be interesting to do a follow up in a couple years time. As always, none of this should be considered financial advice. Please do your own due diligence and don’t take financial advice from a hobby investor.

Cheers.

Good article. Good approach. Wish you well.

An observation you might like to consider: Fundamentals are fine and they indicate the past journey and potential future direction, but it is the quality of management which will deliver the future reality. I feel most comfortable of the future when management have significant skin in the game, have shown recent willingness to invest on market, have their short and long term incentives tied to shareholder returns AND have a proven record of delivering on their outlook announcements.